Scottish Budget 2024 to 2025: distributional analysis

Analysis of the impact on household incomes of tax and social security decisions taken in the 2024-25 Scottish Budget.

Part Two: Analysis of 2024-25 Budget decisions

This part of the document analyses the impact of the tax and social security policy decisions made or confirmed in the Scottish Budget.

It shows the impact on household incomes of:

- A new 45p Advanced rate of Income Tax, applied on income between £75,000 and £125,140;

- Increasing the Top rate of Income Tax by 1p to 48p;

- Freezing the Higher rate threshold at £43,662

- Freezing Council Tax in 2024-25, subject to the agreement of local government.

These are assessed against an assumed 'no policy change' counterfactual. This consists of:

- Uprating most social security payments and tax thresholds with inflation, excluding the Top Rate threshold and the Personal Allowance[7].

- A 5% increase to Council Tax rates (based on the average increase in 2023-24). This is not an indication of what level of funding will be provided to Local Authorities to fund the Council Tax freeze; this is purely a modelling assumption used to estimate household level impacts of the policy.

The full details of the counterfactual scenario are included in the Annex.

Because social security payments have been uprated in line with inflation, and no significant social security policy changes have been introduced in this Budget, the following charts only show the impact of changes to tax policy.

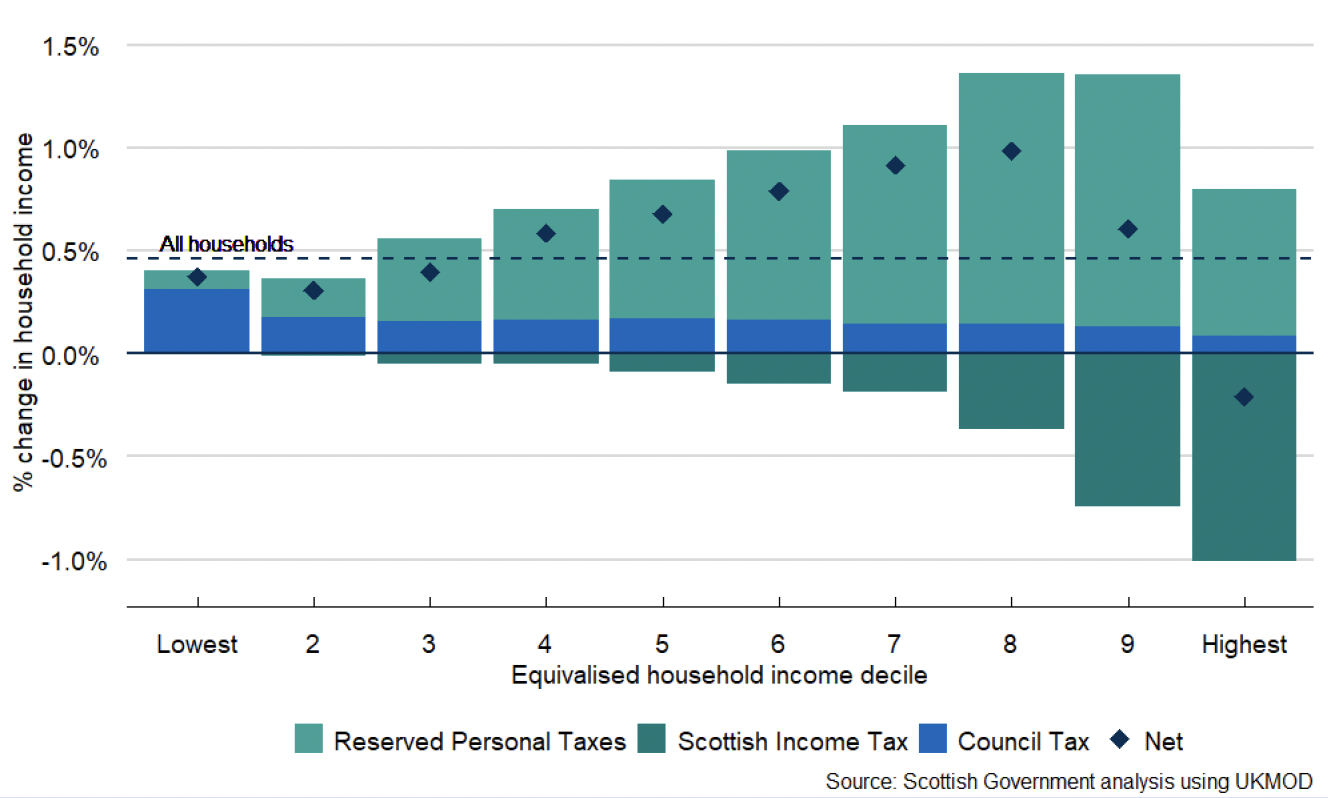

Figures 6 and 7 below summarise the impact of the decisions made in the Budget on household incomes. Impacts are shown as a proportion of net household income and in cash terms.

The freeze in Council Tax generates a small benefit – averaging £57 a year, or about 0.2% of household income - for households in every decile.[8] In cash terms, the benefit is greater for higher income households, who tend on average to live in larger houses and therefore pay a higher rate of Council Tax. However, relative to household income, the benefits of the Council Tax freeze are greatest for the lowest income decile, smallest for the top income decile, and similar for most other household income deciles.

The Income Tax policy is strongly progressive, with the greatest impacts – equivalent to 0.9% of annual household income – on the top two deciles, with lesser impacts on lower income deciles. Principally due to the freeze in the Higher rate threshold, which impacts individuals earning more than £43,662, a small number of households in the lower half of the income distribution are also affected by the Income Tax policy.

However, looking at the Council Tax freeze and Income Tax policy together, the freeze in Council Tax – on average – offsets any negative impact of the Income Tax policy for households in the lower 60% of the income distribution. The negative impact of the Income Tax policy is also reduced for higher income households.

Taking the two policies together, 79% of Scottish households will be paying no more tax as a result of Scottish Government policy changes in this Budget. Of the 21% of households paying more tax, two-thirds of these are in the top two income deciles.

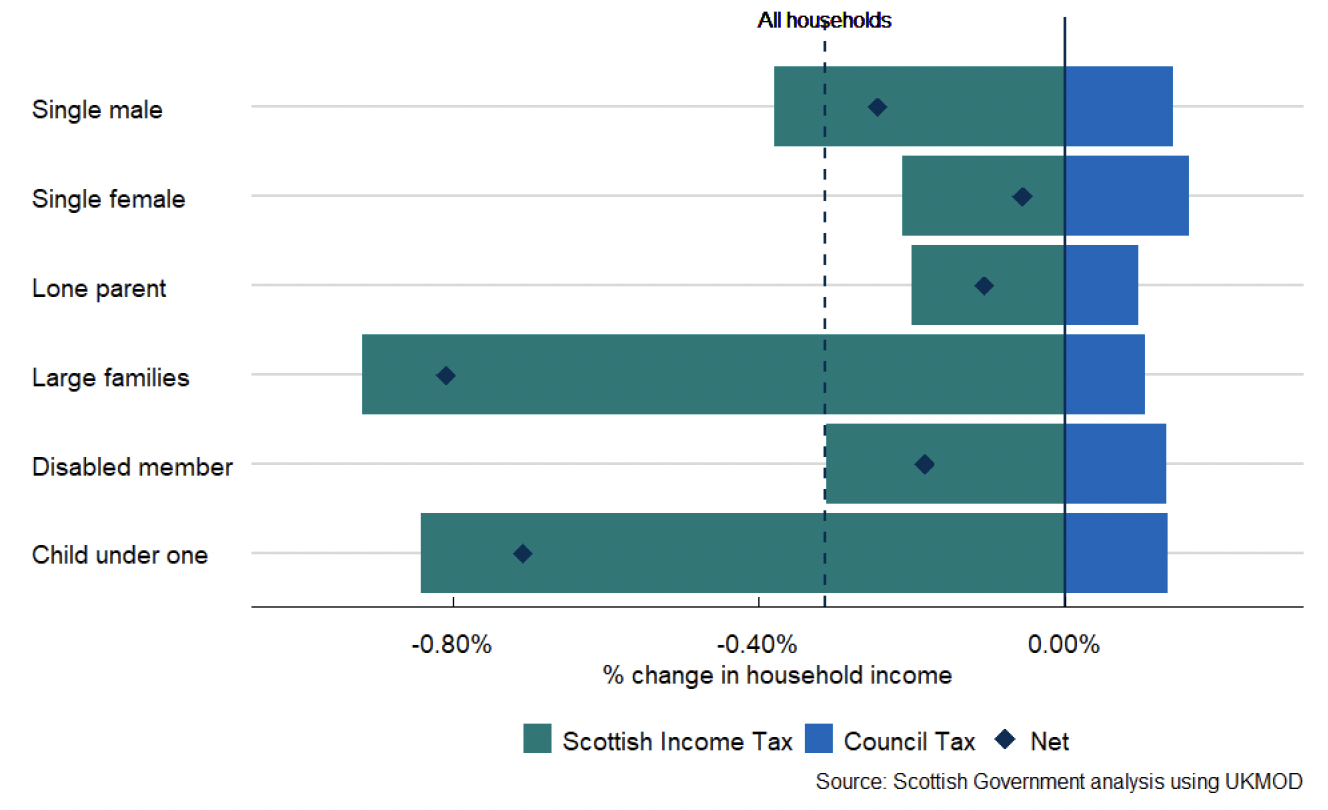

Figure 8 also analyses the impact of the policy changes announced in this Budget by the same household types as used above.

Box: Impact of changes to National Insurance Contribution Rates

This analysis focuses on devolved taxes, where the Scottish Government has power to set policy. However, household incomes will also be affected by recent changes in UK Government policy over reserved taxes and social security payments.

One significant change announced by the UK Government at the Autumn Statement 2023 was a reduction in National Insurance Contribution (NIC) rates paid by both employees and the self-employed.

Figure B1 below shows the impact of these measures on Scottish households alongside the Scottish Government's tax policy changes.

For employees, the NIC rates are reduced by 2% on all earnings between £12,570 and £50,270. This results in a maximum benefit of £754 per year received by all employees earning at least £50,270.

Relative to household income, this results in households in the eighth and ninth income deciles receiving the greatest benefit. The benefit is lower for the top decile, and progressively lower for each lower income decile.

If Scottish and UK Government tax policy changes are considered together, almost all households will be better off due to policy changes announced in the Autumn Statement and Scottish Budget. Only 6% of households – almost all in the top decile – will be worse-off as a result of these changes, on average seeing their income reduce by 0.2%.

The pattern shown in figure 8 largely reflects differences in earnings between household types. For example, the higher impact for single males than single females is driven by the well-documented gender pay gap between men and women.

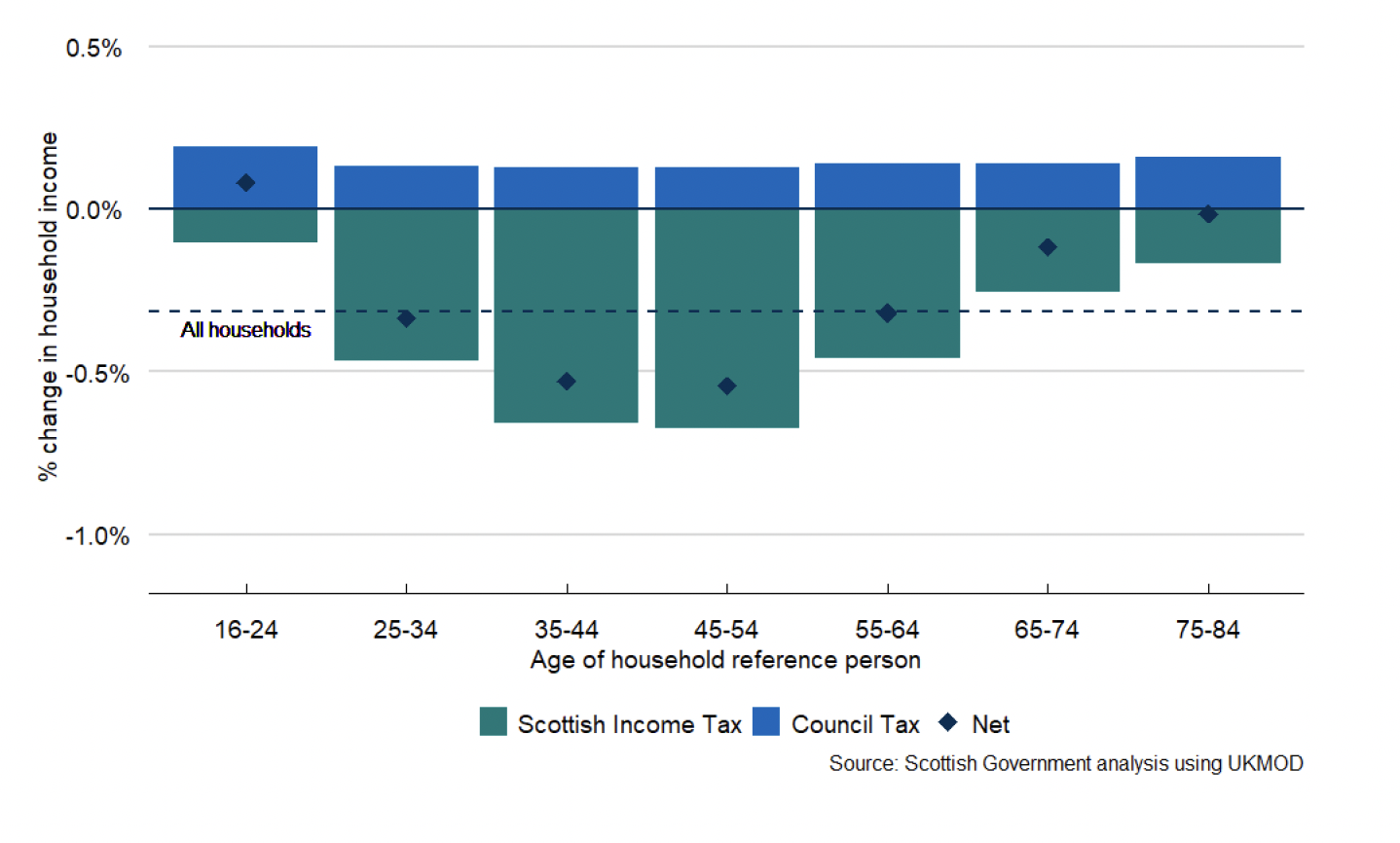

Figure 9 below shows the impact of the Budget policy package by the age of the household reference person. As discussed in part 1, the differences in impact arise from differences in earnings across age groups. The impact of the Council Tax freeze does not vary significantly across age groups.

Contact

Email: angus.hawkins@gov.scot

There is a problem

Thanks for your feedback