Fairer Council Tax: consultation analysis

Analysis of responses to the Fairer Council Tax consultation.

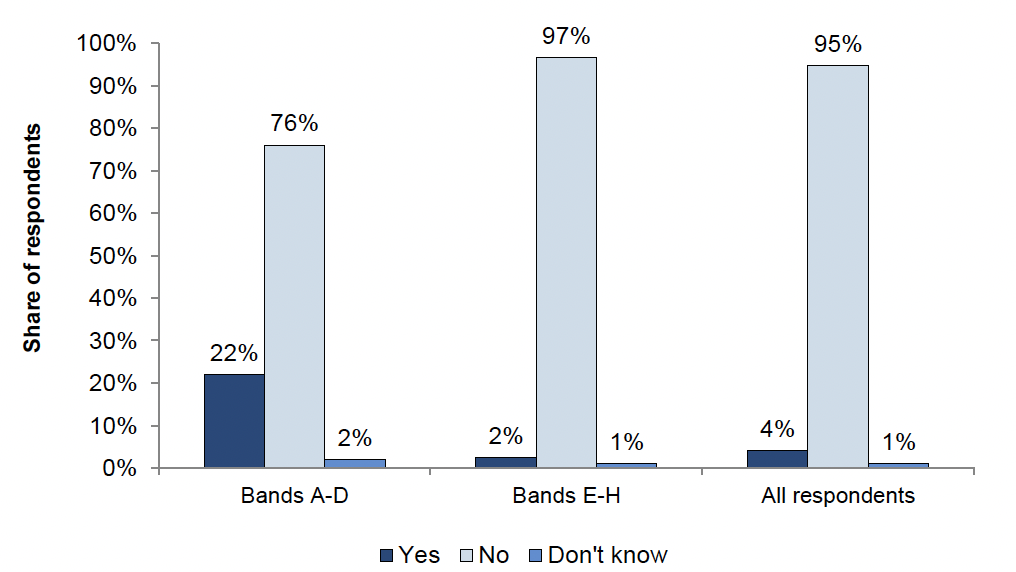

Analysis - Question 1: Do you think that Council Tax in Scotland should be changed to apply increases to the tax on properties in Bands E, F, G, and H?

Quantitative analysis

- There were 14,714 responses to this question (1,321 from Bands A-D and 13,393 from Bands E-H).

- Out of all responses, 95% of respondents did not agree with the proposed tax increase, 4% agreed, and 1% did not know.

- A greater proportion of respondents in Bands A-D agreed with the proposed tax increase (22%) compared to respondents in Bands E-H (2%).

- A smaller proportion of individuals agreed with the proposed tax increase (4%) compared to organisations (20%).

- Out of 15 councils responding the consultation, 67% (10 councils) did not agree with the proposed tax increase, 27% (4 councils) agreed with the proposed increase and 7% (1 council) responded “Don’t know”.

Qualitative analysis

There were 14,557 respondents to the free-text question, which asked respondents to give reasons for their answer. Respondents who agreed with a proposed increase typically mentioned the same key themes and concerns as respondents who disagreed with a proposed increase.[9]

Proposed increase in Council Tax would be unfair

The most common theme raised by respondents was that the proposed increase was unfair, as respondents thought that Council Tax bands did not act as an accurate measure of one’s ability to pay a higher tax rate. In particular, respondents believed that a property’s value did not always align with an individual’s current income level. Many individual respondents discussed their own personal experiences to emphasize this point.

“There is a fundamental misconception that council tax banding is linked to wealth or affordability. This, however, is wildly inaccurate. Council tax banding relates only to the size of the property and not the means of the occupant.” (Individual, Clackmannanshire, Band D)

“There are many homeowners who purchased their home when prices were significantly lower than they are now. At this point in time, actual property values between bands A-H were much closer. […] My household income has decreased since I bought my house over 25 years ago. I cannot afford to pay Council Tax charges based on the value of property that I could not afford to buy today.” (Individual, City of Edinburgh, Band G)

“[…] The value of someone’s property and/or the council tax band they are in are not direct correlations to their income. We believe that these proposed increases could result in lower-income households paying a higher proportion of their income on council tax, further burdening those who are already in a financially vulnerable position. We argue that as households can be asset rich but income poor.” (Organisation)

For example, some respondents pointed out that house prices could be related to geography (these respondents thought that prices for properties in all bands would be lower in rural areas or working-class communities).

“Bands don't mirror very closely the actual income and spending capacity of owners or residents in lots of areas of Scotland […] lots of houses in rural areas or in various zones of lower-income cities, such as Dundee or certain parts of Glasgow […] have relatively low prices. This means that being the owner or resident of a relatively good and large home in Scotland doesn't correlate straightforwardly at all with being a high earner. If you tax way more the houses in those bands, you often won't tax people who are rich, only people who got houses in those bands because the houses were relatively cheap.” (Individual, Dundee City, Band G)

Some individual respondents thought that their hard work (saving over many years to buy a home) was being unfairly punished by the proposed increase.

“I worked hard for 40 plus years and made sacrifices to buy my home, missed out on holidays, luxuries, etc. and now the Scottish Government wants to penalise me.” (Individual, Fife, Band F)

Other individual respondents thought the proposed increase was unfair as they did not utilise council services.

“As a professional couple with no children in a band F property, we are already overcharged as we use very little of the council and utility services council tax goes toward, yet we are expected to pay more because of the ridiculous scenario that we must be using more of said utilities and services just because of the size/value of our property.” (Individual, Glasgow City, Band F)

Proposed increase in Council Tax would disproportionately impact specific groups

Respondents cited specific groups who they believed would be disproportionately affected by an increase in Council Tax among these bands. The groups most frequently mentioned were pensioners, lower-income households and other “asset rich, cash poor” households. Respondents typically argued that although pensioners were once able to afford purchasing a property in a higher tax band, they now earned a fixed income. As a result, these respondents thought that while pensioners might own a property of high value, their current income might not be sufficient to cover a corresponding increase in tax. This view was often held by individuals in Bands E-H.

“The premise that those in bands E-H can afford to pay more council tax, fails to take into account the financial reality of many of these households or the inequalities that exist [in] current banding. […] Many of the properties in my constituency are occupied by those on a fixed income (state pension, etc.) who will lack the ability to find additional income to pay for these rises, on top of increased energy costs for example.” (Organisation based in Fife)

“The substantial increase will affect householders who may be asset rich and cash poor in terms of their properties being higher assessed but who have no savings or fixed incomes from pensions/lower/reduced incomes.” (Individual, City of Edinburgh, Band F)

Similarly, respondents believed that lower-income households could also live in bands E-H properties (for example, these households could have inherited a higher band property or moved to an area with lower house prices across all bands).

“[…] we live in a higher band property and currently live on a low income. My partner's work has been badly affected by Covid and my work is not highly paid. […] The only reason we live in a higher band property is that we moved areas (we could not afford to buy a bigger property with a garden in the area we lived previously) and house prices are lower where we bought. […] We are already struggling to keep up with all our bills each month with the cost of living crisis and an increase in council tax for us would have a significant negative impact on our ability to stay afloat.” (individual, Fife, Band E)

Other respondents thought that the increase could potentially have the greatest impact on middle-income earners rather than high-income earners who could more readily afford the increase. This view was held mostly by individual respondents discussing their own personal experiences.

“Our house was a band D when we bought it, it was not until the paperwork was completed and the local council checked paperwork that they changed it to a band E based on footprint of the property […] Increasing our council tax would mean yet more pressure on us middle earners that make enough to not get benefits, but don’t make enough to comfortably absorb all these cost rises.” (Individual, Dumfries and Galloway, Band E)

Finally, respondents raised potential concerns that the proposed increase could negatively impact larger families (as they would need a larger home to meet their needs) and single parents (who might find it even more difficult to adjust their household spending in response to the proposed increase compared to households with additional earners or other forms of support).

“We are also concerned that this increase in council tax rates may lead to larger families being burdened as they will need a larger home for their needs. This may lead to larger families accruing council tax debt or being forced to move into a smaller home which is unsuitable for their needs.” (Organisation)

“The opportunity to move into smaller properties locally is simply not an option in today's housing market in Scotland. People with larger families require a larger home. They often make sacrifices in other areas to afford their home [...]” (Individual, South Lanarkshire, Band D)

“[…] Council Tax has never been fit for purpose as a method of taxation. It makes an assumption that the size of a person's house is directly correlated to their wealth and ability to pay tax. This is certainly not true for many sections of society for example […] single parents who may have found themselves living alone, single income, in a house as part of a divorce settlement again living in a house beyond their means to purchase […]” (Individual, Scottish Borders, Band G)

“Several years ago my marriage broke down and I have become a single parent. I have been able to afford to stay in what was the family home to try and provide some ongoing stability and security for my daughter, however it has been extremely difficult and can be a challenge at times. […] I am not a high earner and with the current cost of living situation and every household bill on the rise, increasing council tax bills on an 'assumption' that people can afford it because of their address is both unfair and irresponsible of the Government.” (Individual, West Dunbartonshire, Band E)

“Single parents, the majority of whom are women, often find themselves in the position of struggling to cover mortgage costs or rent in higher band properties. As well as this they need to cover essential bills such as council tax on one, normally low, income without any support following the breakdown of relationships. This situation affects the whole family as the single parent has to adjust to budgeting on a reduced income.” (Scotland-wide organisation)

Need for further review or alteration of the Council Tax system

Most respondents who mentioned the need for further review or alteration of the Council Tax system recommended adjustments in the way Council Tax was levied. In particular, respondents who disagreed with the proposed increase often thought that the increase was only a temporary solution and did not address more fundamental issues with the Council Tax system. The most common suggestion (proposed by both individuals and organisations) was to link Council Tax to current income.

“A fair and reasonable council tax charge is far more related to disposable household income than to the value of the property they inhabit. […] I don't dispute that those who are wealthier should pay more, but only suggest that the means of identifying their ability to pay should be assessed on more than property value/band in isolation.” (Individual, Fife, Band F)

The second most common suggestion, mostly raised by individual respondents, was to modify Council Tax so it was levied based on use of services (or replace it with a new tax based on use of services). Respondents suggested that this could be implemented by taxing households based on the number of individuals in the household older than 16 (or 18) and not in full-time education, number of earners or number of residents in the property.

“If a change of council tax rate is needed it, then the whole way that council tax is calculated should be reviewed and changed. Simply basing it off the ‘value’ of a property in my opinion is not a true reflection on what that property and its occupants consumes from the Local Council in services.” (Individual, Aberdeenshire, Band G)

"Council tax burden should not be tied to the value of the property. Council tax is levied for the maintenance of roads, provision of education, waste refuge etc. The amount of waste generated per household is not intrinsically linked to the burden upon the council in terms of key public spending obligations listed above. It is however linked to the number of persons residing or able to reside in the property." (Individual, Aberdeenshire, Band G)

“If anything, council tax should be replaced with a tax on number of persons within the household who are 16 or older and not within full time education. The more people like this within a household means a greater household income (wealthier) and greater use of services (cost to councils). Therefore it's fairer for them to pay more.” (Individual, South Lanarkshire, Band F)

Compared to the number of respondents who suggested modifying the Council Tax system, a smaller number of respondents recommended replacing Council Tax with a new tax. Most of these respondents were organisations. In general, these respondents did not use their answer to explain how the new tax would differ from Council Tax other than the specific tax base. Respondents most commonly suggested a property tax or local income tax as more progressive replacements for Council Tax.

“Making further changes to band modifiers now in the absence of revaluation and further-reaching reform will exacerbate some of the issues inherent in the system and require Council Tax Reduction (CTR) to do even more work to compensate. This is not the way a well-designed tax approach should operate. […] Design of Council Tax’s longer-term replacement, likely based on proportionate property value (potentially with a land component) should commence immediately so that the Scottish Government is in a position to begin consultation on the proposed new design by 2026.” (Scotland-wide organisation)

“More broadly we believe the present council tax system does not meet the needs of a Scotland where tax should be based on ability to pay. We agree the council tax system in Scotland needs to be reviewed and be replaced by a fairer system. Property is the most valuable type of wealth held by households in Scotland, making property taxation a natural starting point for improving wealth taxation. Any reforms or replacement of the Council Tax must tax property wealth more fairly and seek to contribute towards gender equality.” (Scotland-wide organisation)

“If fairness and ability to pay are the criteria for a revised system of local authority finance, Council Tax should be abolished and replaced by a local income tax. There are many people with modest incomes living in larger properties and the size of the property is a poor method of assessing the current income of its residents.” (Individual, Glasgow City, Band F)

Some respondents also suggested increasing the role of Local Councils in administering and defining Council Tax in their jurisdiction.

“[…] Local authorities should have complete control over their local tax - including the rates, bands and form of the tax. This would allow individual councils, should they choose, to retain, reform or replace council tax with another form of local taxation, such as a land value tax. Crucially, this would be a decision about a local tax made by a local authority for its local area, taking into account local circumstances and priorities.” (Organisation based in City of Edinburgh)

Proposed increase would be unaffordable due to cost of living crisis

Respondents frequently mentioned that they believed the proposed increase would be unaffordable due to the ongoing cost of living crisis, with households facing a combination of higher mortgage rates, increase in energy and food prices as well as overall economic uncertainty. These respondents felt that households were currently struggling to keep their heads above water, and the proposed increase could potentially push them towards fuel poverty, financial security or increased levels of debt.

“The proposals are terrible to bring in during a cost of living crisis, with a number of people who will still be under a mortgage in these higher bands […] who will be facing vastly increased costs from their mortgage, only to be compounded by an additional large increase on the cost of the council tax.” (Individual, West Lothian, Band F)

“An increase of the rates suggested would see my home income reduce further when times are really hard for people. […] A council tax bill rise by the rates proposed could see my annual bill rise by £600 per year which would mean something else would have to give, on top of […] heating costs, solid fuel, food, travel inflation and inflation and mortgage rates this is another burden.” (Individual, Stirling, Band F)

“To increase Council tax for these bands by such huge amounts is totally unjustified and can only cause financial hardship at a time of real difficulty for all households in Scotland caused by the cost of living crisis and the current economic uncertainty […]” (Individual, Scottish Borders, Band G)

“While it is true that the Council Tax Reduction scheme reduces the Council Tax liability of many low-income households, it does not capture everyone in bands E-H who would struggle to pay these increased rates. As such, we are concerned these proposals would put many older households at risk of fuel poverty, financial insecurity, and debt, and reduce their quality of life by cutting their disposable income”. (Organisation)

“The current levels of cost inflation and higher interest rates associated with an overall increased cost of living is impacting across all households and the proposed changes will increase these pressures for some households”. (Organisation based in Dumfries and Galloway)

Validity of Council Tax bands and need for revaluation

Respondents believed that current tax band valuations were outdated given that a general revaluation of the Bands has not occurred since they were first set in 1991, leaving many properties allocated in the wrong Council Tax band. For this reason, respondents thought there should be a revaluation of Tax Bands before an increase in tax was considered (this was the most common theme mentioned by organisations).

“I think the whole Council Tax system should be the subject of a general revaluation. The current system of banding properties on the basis of sales values [in] 1991 badly needs [to be] updated […]” (Individual, Angus, Band E)

“Currently, each Council Tax Band represents a range of capital values at 1 April 1991. This consultation does not address the fundamental issue that a substantial number of properties are in bands that are not reflective of their current value. […] A revaluation and the introduction of new council tax bands would go some way to achieving the Scottish Government’s objective of having a fairer Council Tax system.” (Organisation)

“Making further changes to band modifiers now in the absence of revaluation and further-reaching reform will exacerbate some of the issues inherent in the system and require Council Tax Reduction (CTR) to do even more work to compensate […] Many households who should be paying more will not be, and some who should not be paying more will end up doing so, even after mitigations like CTR. It will also set the Scottish Government and Local Authorities up for substantial problems further down the line when properties are eventually revalued, and when Council Tax payers, many of whom will be on low incomes, find out that they have been paying more than they should have due to inaccurate property value, potentially having done so for many years.” (Organisation)

“If council tax as a system is to remain, the only fair means of using it as a basis of payment is to conduct a full property revaluation. [...] I understand that there may not be an appetite for doing this, as it is a huge undertaking. However, failure to do so and simply adding large payments to current bandings is unfair. […]” (Individual, South Lanarkshire, Band G)

Some respondents also recommended that upon revaluing the current tax bands, new tax bands at the top and bottom ends should be added to reflect the current range of property valuations. These respondents believed that adding top-level bands could better account for the overall growth in property prices since 1991, and adding bottom-level bands could help make the tax more progressive.

“We believe a better and fairer way to make the Tax fairer (and potentially raise the additional revenue) is to have regular revaluation of all council tax properties with an increase in the number of bands at both top and bottom end. This would ensure that every dwelling is properly banded and thus then pays the proper share of the tax due. By adding bands at the bottom end and the top end of the valuations also makes the tax fairer and less regressive.” (Scotland-wide organisation)

“[…] I also think that there needs to be an additional band (at least 1) that allows for a more granular distribution of property prices, as well as the top band being designed to only include the small proportion of ‘millionaires' mansions’, potentially based around the difference between median and quoted mean 15 times difference in value between Band A and Band H properties.” (Individual, Perth and Kinross, Band G)

Concerns around provision of council services

Respondents expressed concern about the use by Local Councils of tax revenue to provide adequate services. Of those respondents that brought up this relationship, most expressed a dissatisfaction with the provision of Councils’ services relative to the amount of council tax that was being paid. This view was held primarily by individual respondents.

“As a resident paying council tax, I am seeing less return for my tax and it has been this way for several years. I have seen funding for essential services cut or dropped entirely, and decreased access to local services. […] In short, I do not feel I receive value for money for my council tax and cannot afford to pay further increases.” (Individual, Midlothian, Band B)

Concerns around structure and information provided by the consultation

A small number of respondents expressed concern around the structure of the consultation and the information included in the consultation document. Respondents who raised this theme typically characterised the consultation as too narrow, and inadequate to provide a sufficient review that would be needed to reform the Council Tax system. Some respondents believed that the consultation had focused too specifically on a predetermined proposal (rather than requesting views on Council Tax more generally).

“The purpose of this consultation – in seeking views upon a single proposal to increase the multipliers for Council Tax Bands E-H – is very narrow. […] The narrowness of the consultation severely limits a proper consideration of a range of issues which go to the heart of local taxation (and have been considered on multiple previous occasions with recommendations for improvement), such as its fairness, and its adequacy in supporting local services.” (Organisation based in Scottish Borders)

Other respondents felt that the consultation was based on an incorrect premise (that Council Tax was a regressive tax, the current system was unfair and benefitted owners of higher-band properties).

“The paper does not provide any evidence that there is a correlation between property values and income or between property values and use of or need for services. […] The document attempts to justify its proposals by saying that current rates are lower in Scotland than other parts of the UK. This is irrelevant. Indeed, any valid meaningful comparison would need to take into account the wider context, housing characteristics, and availability and quality of services.” (Individual, Scottish Borders, Band G)

Respondents were also likely to share their disagreements with the Scottish Government, although these were not relevant to the specific consultation question they were asked (and thus not included in the analysis). A smaller number of respondents felt that the consultation had not been sufficiently publicised, did not include sufficient data, cited incorrect data[10] or did not specify how the revenues raised by the proposed increase would be used.

Themes raised by councils

The most common theme raised by councils was need for further review and reform of the Council Tax system. Councils felt that increasing Bands E-H multipliers were too blunt or short term of a tool to make the overall tax system fairer, as they believed the increase would not address systematic issues with the system (in particular failure to link Council Tax to household or occupier income, leading to an unequal approach to valuations).

“Merely altering the multipliers for Bands E-H represents a short-term approach. In our perspective, this approach does not foster equitable taxation through the assumption that residents in Bands E-H possess the means to accommodate these increases.” (Council)

Specific solutions proposed by councils included increasing the number of bands or revaluing property values more frequently.

“[The Council] does not consider that the proposed increases to multipliers for Bands E-H delivers the policy intent of making Council Tax fairer. Expanding the range of Bands to increase the number of lower and higher bands would generate additional revenue and provide a fairer tax system The system of revaluation every 3 years for Non-Domestic Rates ensures valuations are current, generates revenue, and is workable. A similar system of revaluation for Council Tax would deliver similar benefits.” (Council)

Councils also mentioned the impact that cost of living pressures (including increases in mortgage rates, energy costs and inflation) had on household incomes. As a result, these respondents believed it would be unfair to increase Council Tax on some households in the midst of these pressures. Some of these councils thought that the Council Tax Reduction scheme would be insufficient to support taxpayers and called for an increase in CTR grant allocation and widening of CTR income eligibility criteria.

“The response from the Council is subject to caveat with the affirmative response being dependent on there being […] a widening of the CTR income eligibility criteria to enable those households that will be significantly impacted by the new multipliers to apply for and be awarded CTR. This is particularly relevant to those households that are in Council Tax Band E.” (Council)

Several councils also believed that revenues raised by the proposed increase would not be retained by the local authority (which they viewed as negatively impacting local residents who would not benefit from the increase), or that the proposed increase would lead to a reduction in the general revenue grant from the Scottish Government.

“When the previous change was made to the multipliers in 2017, the whole sum came to local authorities. Our assumption is that this is the intention with the present proposals. If this was not the case, and the additional monies raised were intended simply to shift the balance of council income from central to local funding, not only would the impact be marginal (effecting no meaningful change in the relationship between taxation and local empowerment), it would in no way address the issue of council funding adequacy/sustainability.” (Council)

Four councils also expressed concern that the proposed increase could impact tax collection levels:

“While adjusting Council Tax multipliers could yield increased revenue, it remains essential to question its collectability. Councils must also factor in provisions for potential bad debt and the associated collection expenses.” (Council)

Finally, four councils agreed that the proposed increase would provide additional revenue to address budget gaps and increase service provision.

“Any increase to the multipliers provides the ability to raise much needed income for local authorities to support local services.” (Council)

Contact

Email: ctconsultation@gov.scot

There is a problem

Thanks for your feedback