Modelling impacts of free trade agreements on the Scottish economy

This report explores the modelled impact of several free trade agreements on the Scottish economy, including the UK–EU Trade and Cooperation Agreement. It considers the impact on the economy as a whole, as well as at a sectoral level, utilising Gravity modelling and Computable General Equilibrium.

Differential impacts

Trade liberalisation can benefit the economy through greater specialisation, higher productivity, and higher levels of economic activity.

As trade barriers are removed, businesses benefit from greater access to international markets, firms are encouraged to enter new markets, and trade increases. This tends to raise productivity across the economy, resulting in higher earnings for workers.

However, trade also exposes domestic firms to import competition which may reduce demand for domestic goods and services. In response, domestic industries are required to adjust: either becoming more productive and competitive, or risking loss of market share and profitability, with associated impacts on workers and the communities where these firms are based.

In other words, trade liberalisation causes a restructuring in the economy – some sectors gain and others lose. This has implications for workers as well as businesses.

To understand the distributional impact of trade scenarios on workers, the estimated impact on sectoral employment from the CGE model is linked to the additional data on sectoral employment by characteristics. The impact can be different across characteristics such as gender, ethnicity, disability, age, and others.

As an initial exercise, this section considers the impact on female and male workers. We also look at regional impact of the scenarios. We do not consider the impact on consumers through changes in prices and availability of products as a result of trade policy changes, although this is also an important channel of impact on households. Further work in this space could explore feasibility of producing labour market impact breakdowns for other characteristics, smaller geographies, and consumer impacts with the data available for Scotland.

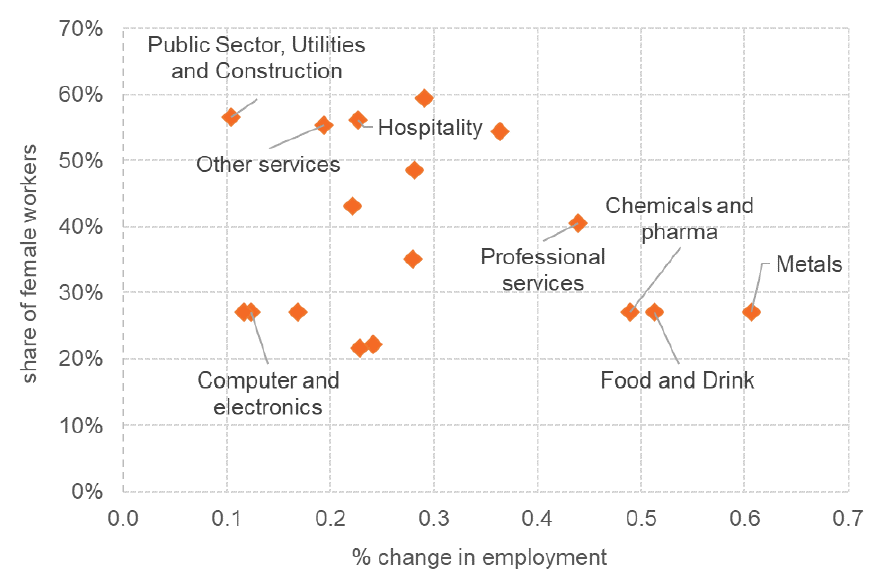

First we look at the labour market impact of Scenario 1 – trade liberalisation with non-EU partners. Figure 14 shows that employment increases the most in relative terms in manufacturing of metals, which tends to have a low proportion of female workers. Sectors with a higher proportion of female workers (such as Public Administration, Education, and Health combined with Utilities and Construction, Other services, Hospitality) generally tend to see smaller increases in employment relative to the baseline. This finding is not surprising as tradeable sectors tend to have a lower share of female workers.

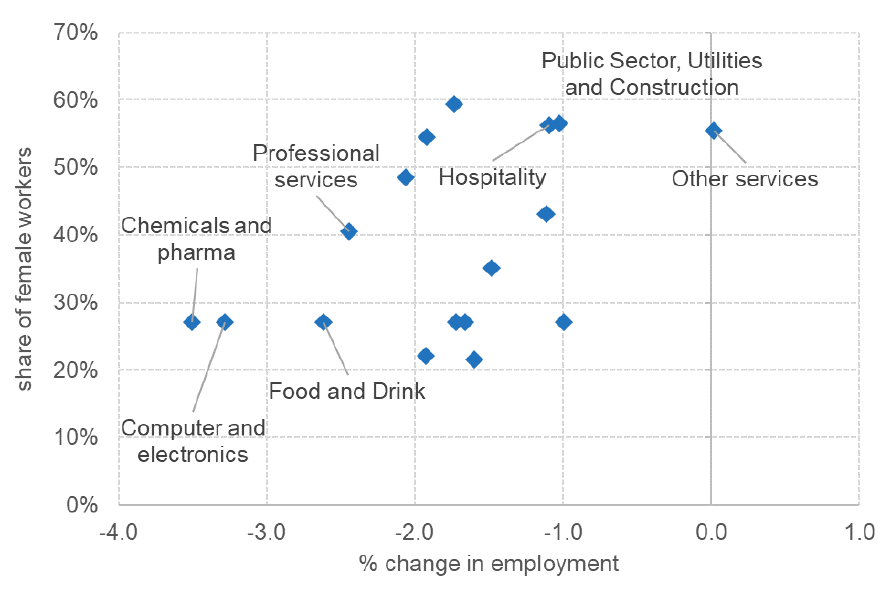

Figure 15 shows the combined impact of the four non-EU FTAs and the UK–EU TCA on sectoral employment alongside the share of female workers. It shows that sectors that see the largest decreases in employment tend to have lower shares of female workers. This may suggest that industries with a large proportion of male workers may be impacted more negatively by the UK–EU TCA.

Source: CGE modelling and ONS employment data

Source: CGE modelling and ONS employment data

Another way in which our scenarios could affect different groups of people differently is through varying impacts across regions of Scotland. To investigate this, we have used the sectoral percentage change in employment as above, and combined this with data on employment in each region by sector, from the ONS Business Register and Employment Survey. This allows us to estimate the impact on employment by region in our scenarios.

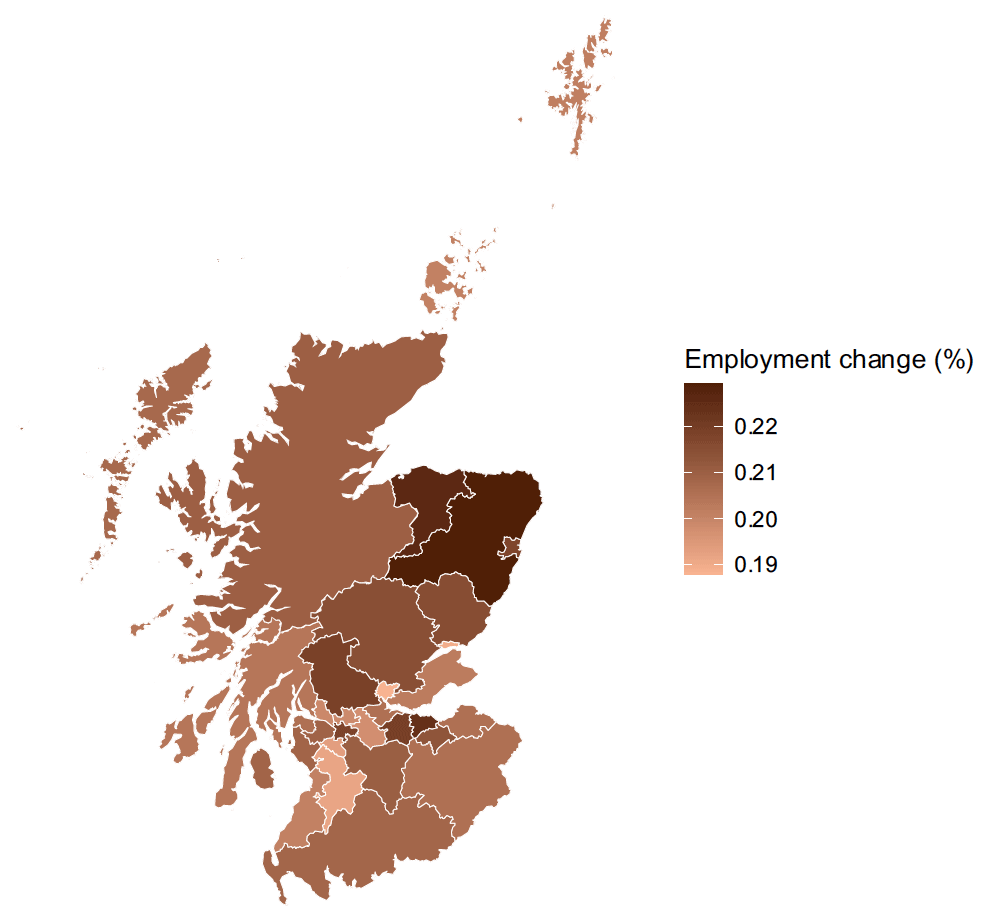

Figure 16 shows the employment change by region in Scenario 1: the four non-EU FTAs. All regions experience an increase in employment, with employment in the North East of Scotland and parts of the Central Belt increasing the most, and Dundee, East Ayrshire, and Clackmannanshire increasing the least. However, the differences between regions are relatively small, with all increases in employment being between 0.19% and 0.23%.

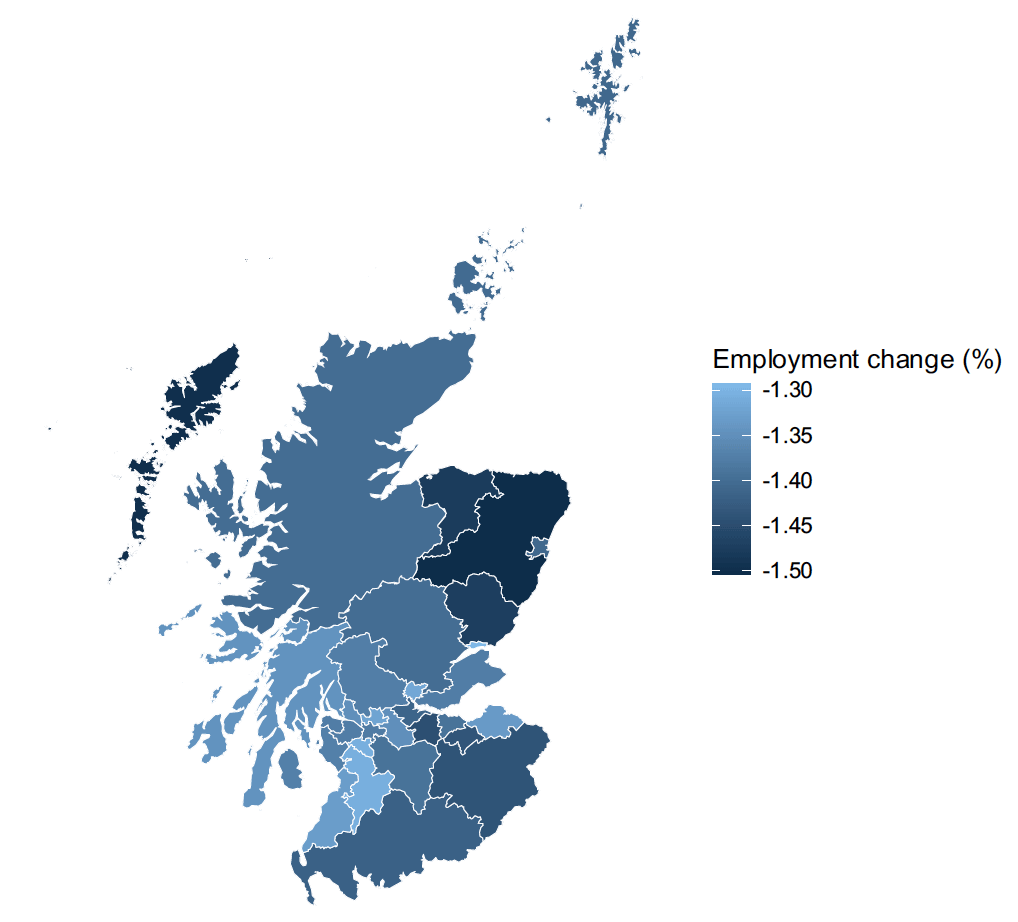

Figure 17 shows the employment change by region in Scenario 2: the non-EU FTAs and the UK–EU TCA. All regions experience a decrease in employment. The pattern is similar to that seen for Scenario 1: the North East experiences the largest decrease in employment, while Dundee, Clackmannanshire, and areas around Glasgow experience the smallest decrease. The decreases are all between 1.3% and 1.5%.

The sectors most affected by Scenario 1 are Metals, Food & Drink, and Chemicals & Pharmaceuticals. The regions whose overall employment is most affected by Scenario 1 tend to be above average in terms of employment share in these sectors.

The sectors most affected by Scenario 2 are Chemicals & Pharmaceuticals, Electrical Equipment, and Food & Drink. Employment share in these sectors is concentrated in the North-East, which is the region most affected by Scenario 2.

Source: SG OCEA CGE modelling and ONS employment data

The map shows greater employment increase in the North East and parts of the Central Belt, and smaller employment increases in local authorities such as Dundee, East Ayrshire, and Clackmannanshire.

Source: SG OCEA CGE modelling and ONS employment data

The map shows greater employment decrease in the North East, and smaller employment decrease in Dundee, Clackmannanshire, and areas around Glasgow.

Contact

Email: EUEA-SG@gov.scot

There is a problem

Thanks for your feedback