Publication - Research and analysis

Scottish economic bulletin: January 2025

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Business Conditions

Business activity has continued to grow in the second half of the year though the pace of growth has eased.

Business Activity

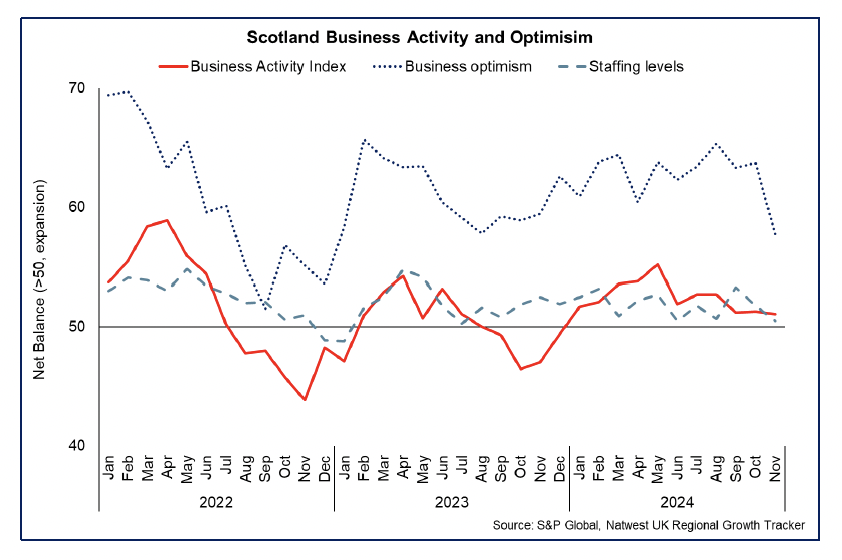

- The RBS Growth Tracker business survey indicates that business activity in Scotland’s private sector continued to grow in November (51.1) maintaining the pattern of positive growth in 2024, albeit more moderately than earlier in the year.[4]

- However, the indicator was down marginally from October and fell to its lowest level in 2024 to date. This reflects that the pace of activity growth has eased in the second half of the year, with activity in the manufacturing sector remaining weaker than in the services sector.

- Broader Growth Tracker indicators also suggest weaker business activity with new business orders continuing to decline (49.7), albeit to a lesser extent than in the previous month, while business optimism fell to a 23-month low in November (57.7).

Business Concerns

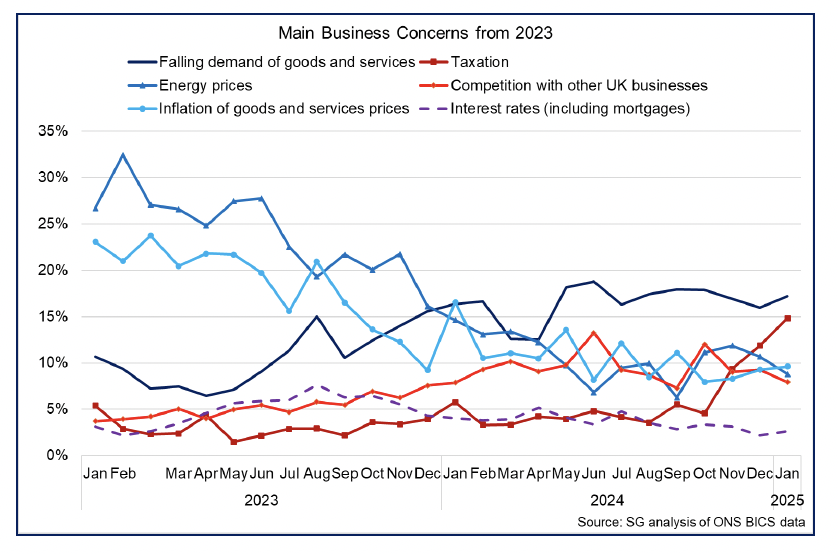

- At the start of the new year, the Business Insights and Conditions Survey (BICS) indicates that falling demand for goods and services remains the leading cause for concern among businesses for January, cited by 17.2% of businesses, up slightly from December and in line with data from the middle of 2024.[5]

- Taxation is the second most commonly cited concern for businesses in January, with the proportion of businesses flagging this issue rising from 11.9% in December to 14.8% in January, and has been on an upward trend since October.

- Concerns around some other issues remain lower than in recent years, with energy prices being cited by 8.8% of businesses (down from 14.6% in January 2024), and inflation also becoming less of a concern, falling to 9.6% from 16.6% January 2024.

Business Costs

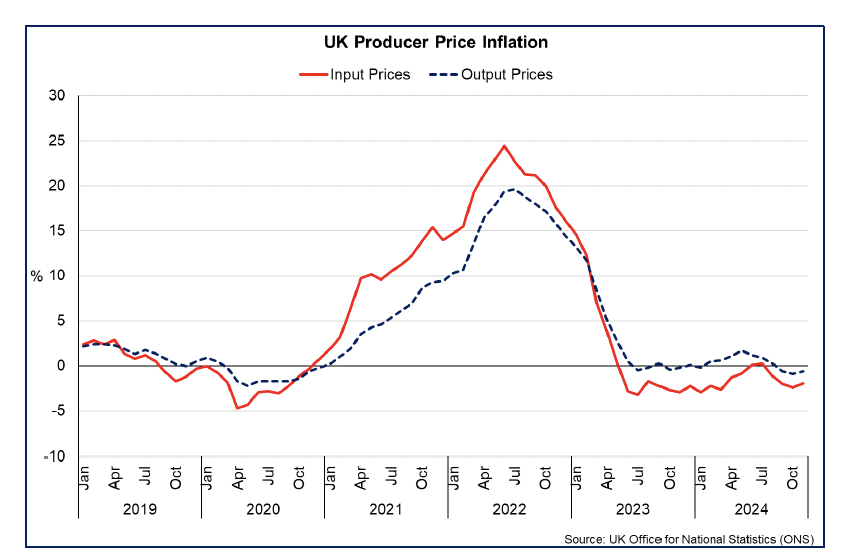

- At a headline level, producer input prices fell by 1.9% over the year to November 2024, up from a fall of 2.4% in November. The key driver of this was the easing of crude oil price disinflation (down 14.3% annually, compared to a fall of 21.3% in October). In terms of the feed through to output prices, producer output prices fell 0.6% over the year to November, rising from a fall of 0.9% in the previous month.[6]

- More broadly, Scottish business survey data from the RBS Growth Tracker also indicates increased input and output price growth, with the measures in November standing at 60.2 and 55.2 respectively. This indicates that input and output costs are continuing to rise, and at a slightly faster rate than in recent months, with labour, energy and material costs all contributing to cost pressures in recent months.[7]

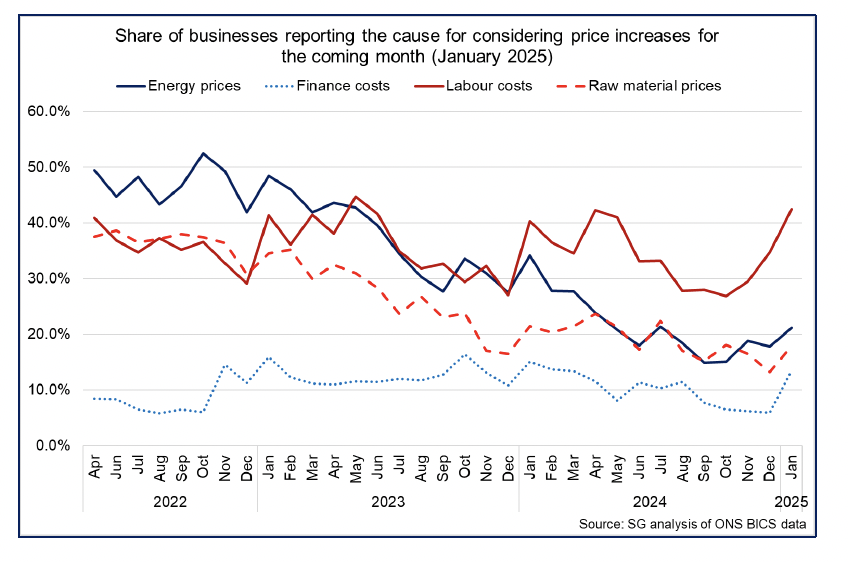

- These factors have also been identified in BICS data for January, showing a recent rise in the share of businesses considering price increases because of labour costs (42.5%), energy prices (21.2%), raw material costs (18%) and the cost of finance (13.6%). 39.3% of businesses responded that they did not plan to increase prices, the lowest figure since May 2024.

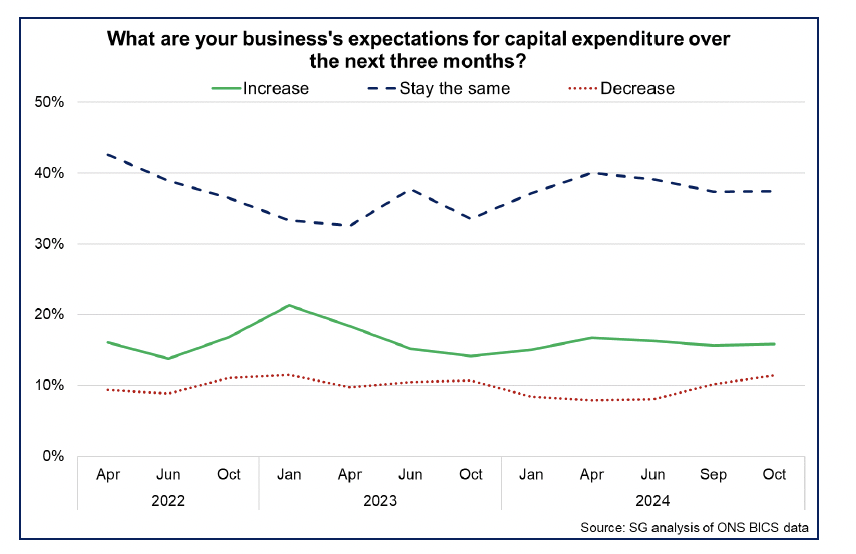

Business Investment

- Latest business surveys for 2024 show that indicators of new capital investment improved from 2023 but remained weak overall with the combination of business concerns around demand, cost pressures and borrowing costs continuing to weigh on business investment decision making.

- BICS data indicate that the majority of businesses continued to expect capital expenditure to remain the same (37.4%) or increase (15.6%) in the final quarter of 2024. However there was a slight increase in the share of businesses expecting to decrease capital expenditure in the second half of 2024 (10.2%), compared to the first half of the year.

- Of those businesses expecting to authorise capital expenditure, 48.1% reported that it would be for replacements, with fewer respondents intending to provide new services ( 6.8%) or purchase new technology (8.4%). Business investment is also being directed to increase efficiency (18.3%) and expand capacity (15.1%).

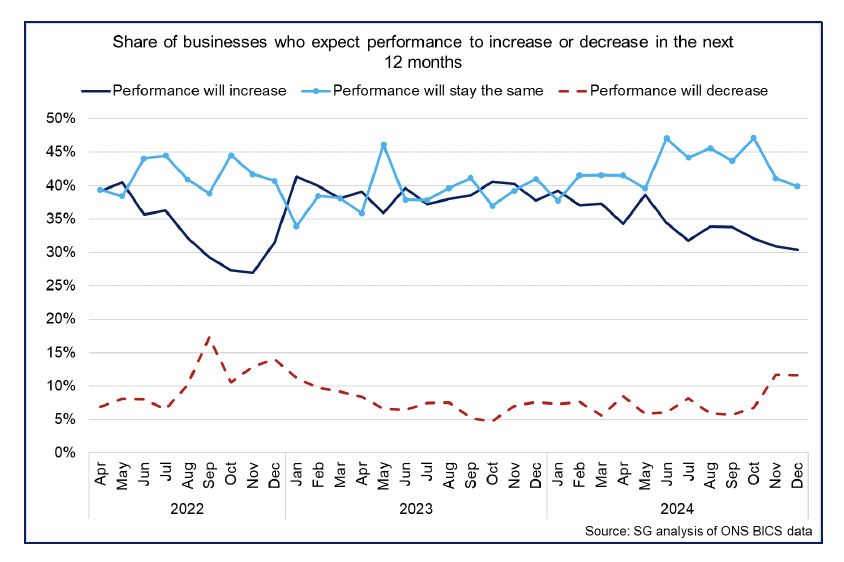

Business Optimism

- As outlined above, RBS Growth Tracker data shows that business optimism in Scotland fell sharply from October (63.7) to November (57.7), albeit remained positive.

- Similarly, BICS data for December showed a softening in business sentiment, with the share of businesses expecting performance to improve (30.4%) or stay the same (39.9%) falling from previous months. The share of businesses expecting performance to worsen has also increased in recent months, but has remained broadly stable from November to December at 11.6%.

Contact

Email: economic.statistics@gov.scot

There is a problem

Thanks for your feedback