Scottish Housing Market Review Q4 2024

Quarterly bulletin collating a range of previously published statistics on the latest trends in the Scottish housing market.

8. Mortgage Arrears and Possessions

8.1. Arrears

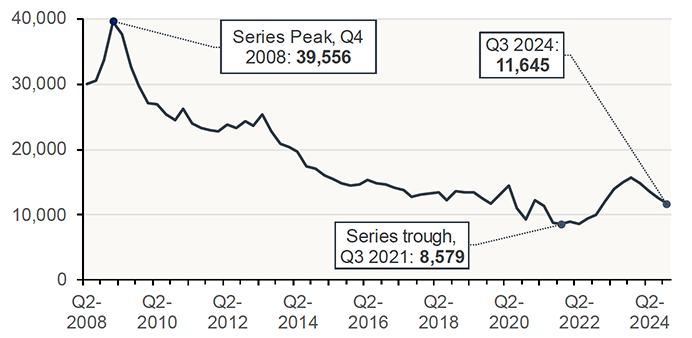

As shown in Chart 8.1, following a peak of 39,556 in Q4 2008 during the financial crisis, there was a long-term decline in the number of regulated mortgage accounts entering arrears across the UK, which continued during the Covid period, reaching a trough of 8,579 in Q3 2021.[5] This was followed by a steady increase over the next three years, with accounts entering arrears reaching 15,705 in Q3 2023. However, this has been followed by 4 consecutive quarterly declines, with 11,645 regulated mortgage accounts entering arrears in Q3 2024.

Source: FCA. Includes both securitised and unsecuritised loans.

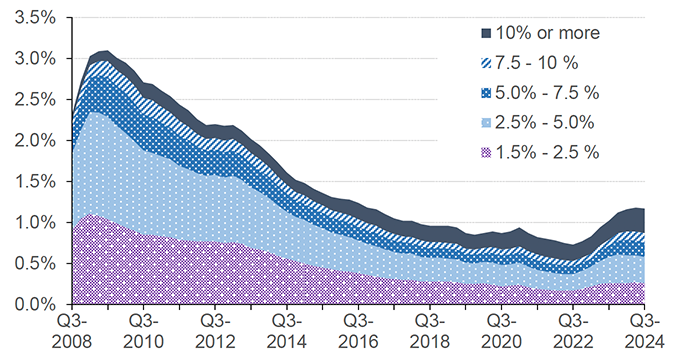

Chart 8.2 plots the share of lenders' outstanding balances that were in arrears by degree of severity. The share of lenders' outstanding regulated mortgage balances that were in arrears of more than 1.5% of the outstanding loan balance stood at 1.2% at the end of Q3 2024. The stock of mortgages in arrears has stabilised in recent quarters as the flow of mortgages into arrears has began to fall, as discussed above.

Source: FCA. Includes both securitised and unsecuritised loans; share is calculated as balances on cases which are in arrears expressed as a % of total loan balances.

UK Finance data shows that there were 17,770 buy-to-let (BTL) mortgages in arrears of 1.5% or more of the outstanding balance across the UK at the end of Q3 2024. This is the third consecutive quarter-on-quarter fall, with the number of BTL mortgages in arrears falling by 9.2% since its recent peak of 19,750 in Q4 2023. BTL mortgages in arrears as share of total BTL mortgages has fallen from 0.99% to 0.91% over this period.

FCA data for non-regulated lending (which includes BTL lending but also some other types of lending, and is collected on a somewhat different basis[6]) shows that at the end of Q3 2024 mortgages which were 1.5% or more in arrears represented 1.37% of the total number of mortgages. While this was up from 1.23% a year earlier, it is at similar levels to the last three quarters, reflecting the decrease in non-regulated mortgages entering arrears in recent quarters.

8.2. Possessions

Over the year to Q3 2024, FCA data shows that the number of new regulated mortgage possessions increased by 248 to reach 968 (up 34.4%). Despite this increase, new regulated possessions remained below their pre-covid levels (the quarterly average in 2019 was 1,318).

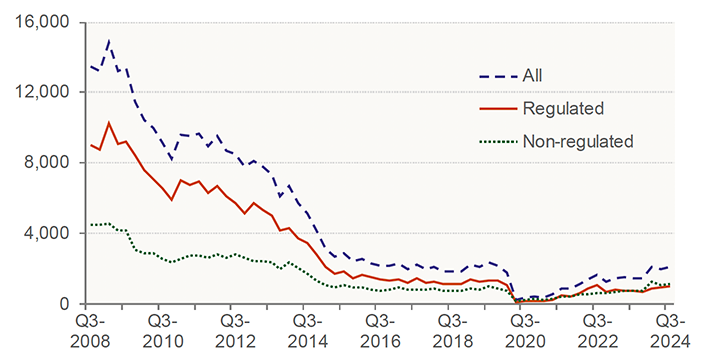

FCA data also show that the number of new non-regulated mortgage possessions rose by 56.9% to 1,016, which was also above their level in 2019 (a quarterly average of 889), although, as illustrated by Chart 8.3, significantly below the levels in the years following the 2008 financial crisis. With respect to BTL mortgages specifically, UK Finance data show that there were 710 BTL mortgages taken into possession in Q3 2024: while the same level as the previous quarter, this was a 73% annual increase, and was also above the pre-covid level (an average of 668 in 2019).

For both regulated and unregulated mortgages, new possessions have been rising to reflect the previous upward trend in in the stock of mortgages in arrears. With the stock of mortgages in arrears now stabilising as the flow of mortgages into arrears slows, new possessions might also begin to stabilise in the coming quarters (as BTL new possessions have done in the last quarter).

Source: FCA

Contact

Email: jake.forsyth@gov.scot

There is a problem

Thanks for your feedback