Climate change - Scottish National Adaptation Plan 2024-2029: business and regulatory impact assessment

Business and regulatory impact assessment (BRIA) undertaken for the Scottish National Adaptation Plan 2024-2029.

Costs and Benefits

This section provides an overview of the anticipated costs and benefits of each option considered. This is largely based on the available literature however contains respective sections informed by the business consultation process.

Benefits

The assessment of benefits considers benefits of both options outlined in the ‘Options’ section of this report, including business as usual (option 1) and the benefits of implementing the adaptation outcomes of the Adaptation Plan (option 2).

Option 1 – Business as Usual (do nothing)

Under this option, it is not anticipated that there will be additional benefits beyond the benefits of the current SCCAP2 that relate to the intended objective. It is also anticipated that there could be a plateau or decline in the scale of benefits from the current SCCAP2 as climate change accelerates, with impacts out pacing current information and actions. Furthermore, failure to update the current SCCAP2 would lead to Scotland not complying with the 2009 Climate Change Act.

Option 2 – Implement the draft SNAP

Under this option, it is anticipated that there will be benefits from the implementation of the outcomes of the Adaptation Plan. The benefits associated with this option have been drawn together from available evidence and analysis from sources to provide high-level estimates of potential benefits.

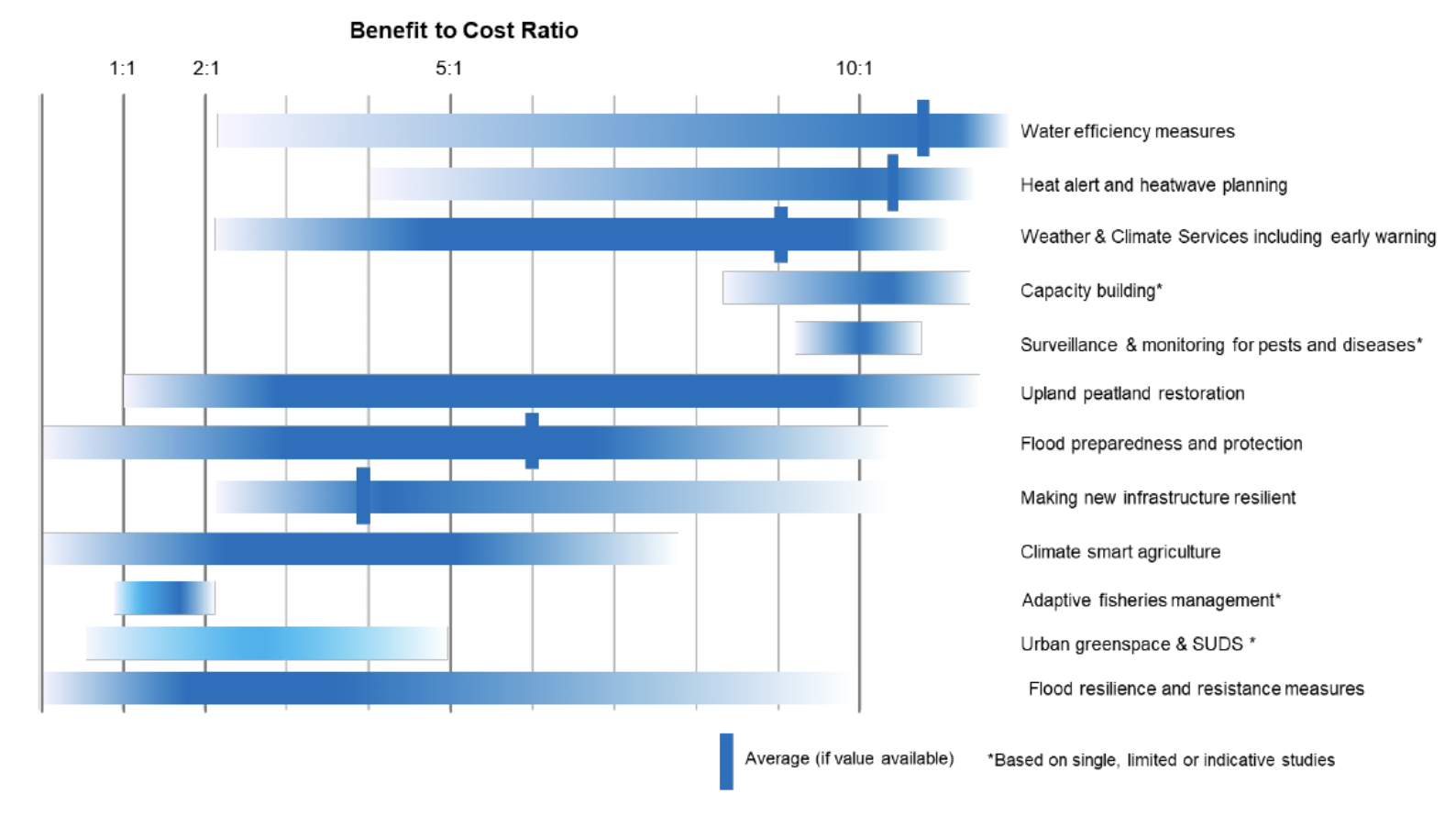

It is anticipated that early adaptation will deliver high value for money. According to an initial review of the benefits of adaptation for the CCRA3, early adaptation investments will lead to economic benefits in addition to important social and environmental co-benefits. The review states that the benefit-cost ratios typically range from 2:1 to 10:1 (Watkiss, 2021).

However, it is likely that the benefits of adaptation will be long-term compared to the costs of adaption, which are likely to include high initial costs for business and people. The same report suggests that every £1 invested in adaptation could result in between £2 to £10 in economic benefits. It is important to note that the outcomes of the Adaptation Plan will have cross-cutting benefits and co-benefits, such as reducing losses from delaying adaptation, which make climate change harder to tackle in the future, potential economic gain, social, and environmental benefits (Watkiss, 2021).

Outcome One: Nature Connects

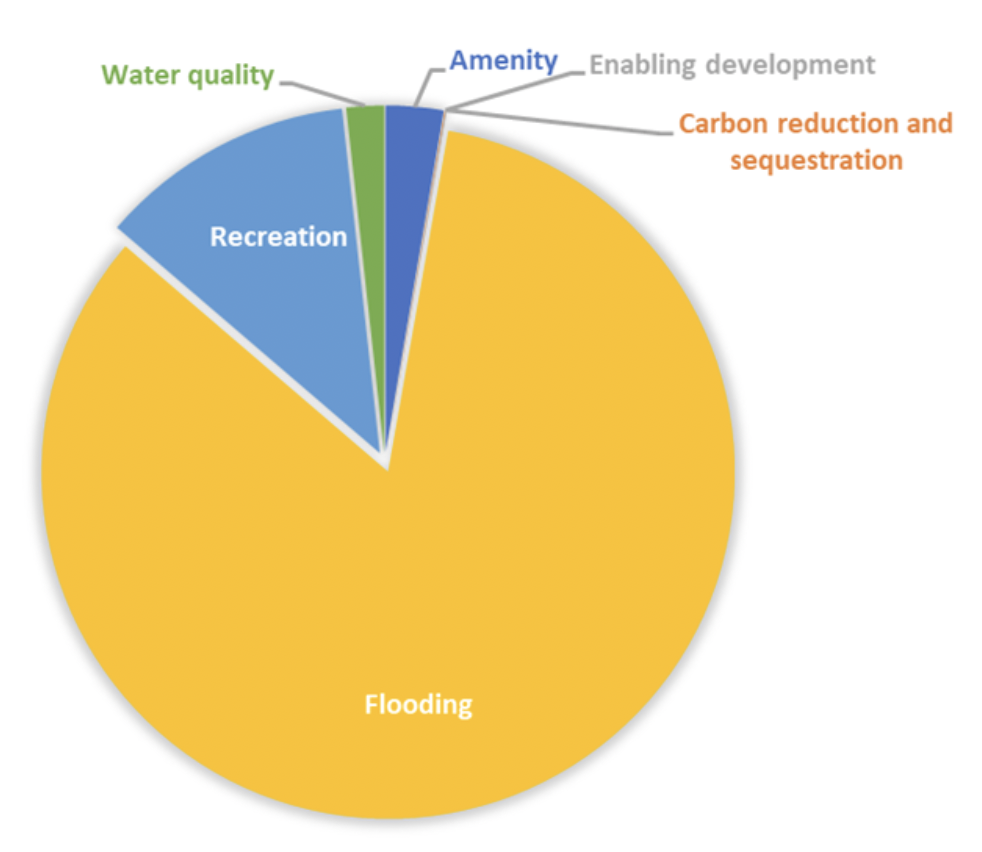

It is anticipated that actions to promote blue-green infrastructure (BGI) and investment will reduce the risk of flooding for businesses and related infrastructure within Scotland’s built environment, as well as create more opportunities for investment in BGI. A city-wide indicative estimation for the potential value of the range of benefits from blue-green infrastructure is provided in a B£ST (Benefits Estimation Tool for valuing the benefits of blue-green infrastructure) case study for Glasgow City Council’s surface water management plan (B£ST, 2019). The tool was used to assess the benefits of delivering SuDS in Glasgow estimated at a total present value (PV) benefit of £70.7 million (before confidence) and £63.1 million (post confidence) for benefits such as flooding, recreation, amenity, water quality, and carbon reduction and sequestration as seen in Figure 2.

It is important to note that the benefits to the built environment extend beyond direct impacts to the built environment, having the potential to have benefits for dependent sectors such as transport and distribution, food and drink industries, health and wellbeing, and Scottish businesses. Indicative estimates also show that for every £1 invested in the Edinburgh’s parks and greenspaces, there is a generated £12 return in social, economic and environmental benefits (Edinburgh Council, 2013) and estimates also place the removal of air pollution by urban green-blue space in the UK at £162.6 million in cost savings for health costs, avoided deaths, and hospital admissions (ONS, 2019).

There are also anticipated knock-on effects between sectors and groups. For instance, actions to promote nature-based solutions into new transport and distribution infrastructure projects will have benefits for businesses and services dependent on transport and distribution networks. Additionally, there is an opportunity to avoid costs of future retrofitting and adaptation by incorporating climate change adaptation into current planning and design.

It is anticipated that actions to promote investment and finance BGI and marine restoration will create more opportunities for investment in BGI in Scotland. This will also bring potential benefits for fisheries in the medium term as well as benefits for coastal recreation and tourism business as a result of nature and habitat restoration and enhancement.

The delivery and uptake of policy, plans and strategies will have direct and indirect benefits on Scotland businesses and sectors. While there is limited evidence on the projected benefits from forthcoming policies like Scotland’s new Water and Drainage Bill, according to the UK Government, an investment of £5.2 billion for new flood and coastal defences in England could better protect 336,000 properties by 2027 however, these figures will vary in relation to Scotland (UKG, 2020). For instance, the new water and drainage bill, Scottish Government’s flood resilience strategy, biodiversity and coastal change adaptation plan, have the potential to reduce flood risk for businesses and public infrastructure. An international city comparison study city-wide estimate in shows that at a cost of up to £85 million for interventions to manage future surface water flooding likely including about 15,000 blue-green infrastructure features such as planted water detention basins and bioswales, permeable paving, street planters and bioretention tree pits, verge rain gardens and rainwater downpipe planters, covering a catchment of about 15 hectares, the investment could generate 385 sustainable jobs and provide additional wider benefits at a present value of more than £30 million (Severn Trent, 2021). The benefits include flooding and water resource management, water quality, carbon storage, climate adaptation, amenity and wellbeing, and urban regeneration.

Modelling suggests a worsening of these risks from more frequent extreme temperatures and extreme weather events. Integrating adaptation and resilience into transport strategies and plans can reduce the risk to businesses, people and supply chains through travel disruptions and the costs of travel disruptions. This also reduces costs to Scotland’s transport infrastructure by avoiding future retrofitting needs in the long-term.

The development of the next Land Use Strategy, the Scottish Wild Salmon Strategy and the Land and Agriculture Just Transition Plan, will help promote natural functioning landscapes and habitats as well as direct monitoring and assessment of Scotland’s salmon which will be beneficial for fishery, agricultural, horticultural and forestry businesses.

The proposed Scottish Plan for INNS surveillance will help early identification and response beneficial for land and marine based industries, including agriculture, fishing and forestry businesses which will have additional benefits for food security and the wellbeing of Scottish consumers; helping mitigate the risks of pests and invasive species with benefits of increased pest resilience of crops and trees for farmers and foresters. The economic and environmental costs of managing established pests, pathogens and INNS are considerably higher than those of biosecurity measures to prevent them from becoming established. Therefore, the Adaptation Plan’s policies and actions focusing on enhanced prevention, monitoring, surveillance, and early response are considered highly beneficial. Increased horizon scanning for INNS and improved coordination with international pest risk surveillance organisations would help Scotland manage risks associated with changes in post EU-exit trade and climate.

Additionally, monitoring and surveillance initiatives can assess opportunities for increases in species populations because of climate change. The CCRA3 states that modelled changes in climate suitability for some bird species showed the largest increases were projected for the north and west, especially in Scotland (CCC, 2021). As such, it can be assumed that climate change will continue to offer opportunities to some species, which can be explored through monitoring initiatives.

Planning and climate change guidance and the new National Marine Plan 2 will provide coordinated adaptation frameworks which could close the information gap, and promote evidence-based decision making for flood risk in Scotland’s sectors such as the transport and distribution sector, and the marine environment. Similarly, the potential creation of a Scotland wide coastal monitoring programme will also lead to co-ordinated adaptation and improved resilience for coastal industries. Analysis suggests that coastal adaptation is extremely cost effective, able to significantly reduce residual damage costs down to low levels (CCC, 2021).

Policies promoting sustainable practices in agriculture and fishing could make Scottish business more competitive in local and international markets as some businesses are under pressures to adopt more sustainable practices.

Additional and continued support is crucial for Scotland’s businesses, especially small and medium scale enterprises (SMEs). Support from the Scottish Government, through local authorities, in mapping opportunities for land use and nature networks will help local authorities and business understand the impact of land use changes on business operations.

The Peatland Action Plan and the review of UK Forestry Standard will create opportunities for green finance investment and peatland contractors, as well as the forestry sector.

Outcome Two: Communities

The Adaptation Plan’s promotion, research, funding and investment, and policy development streamline common standards of resilience and bring together local and regional partners for knowledge exchange, potentially increasing preparedness and investment planning to reduce vulnerability. Non-economic benefits can include improved decision-making for businesses however assessments indicate high economic benefits from investing in flood adaptation infrastructure, according to the CCRA3. Collaboration between the Scottish Government and local government will improve public, private, and third sector co-ordination, and action to support private sector adaptation and resilience. This will be achieved through climate delivery frameworks, and wider and improved partnership to deliver the implementation of the place principle with planning and health benefits. According to the World Economic Forum, collaboration between government, businesses, organisation, and public sector bodies through the delivery of partnerships for climate change adaptation can have benefits for adaptation to extreme weather events, sea-level rise, marine protection, biodiversity loss, private sector engagement and the accessibility and affordability of technical innovations (World Economic Forum, 2020). Additionally, support for local plans like the Regional Marine Plans will improve marine coordination and action to support adaptation and resilience.

The Adaptation Plan’s resilience actions have the potential to support society and businesses become more prepared and better able to respond to climate change and severe weather events.

Flooding remains the most severe climate risk for Scotland and the costliest hazard for Scotland’s businesses according to the CCRA3. The Adaptation Plan objectives, such as improving forecasting services and a flood resilience strategy, will have significant benefits in helping public services, and businesses become more prepared and better able to respond to extreme weather events which can help reduce costs associated with disruption and reducing recovery times. Additionally, reducing flood risks in urban areas lowers financial costs, increases security, and makes investments that would otherwise be too vulnerable to climate risks more viable. For example, indicative estimates in a press release for England suggests that an investment of £860 million in 1,000 schemes could reduce flood risk by 11% and protect 336,000 properties by 2027, avoiding £32 billion in economic damages (UKG, 2021).

The Adaptation Plan commits to engage with FloodRe to ensure that flood insurance remains affordable to those at risk. Any engagement to ensure flood insurance remains affordable is beneficial for businesses to remain competitive in areas most at risk of flooding through asset protection and reduced operational costs. Furthermore, affordable insurance costs have the potential to foster innovation and growth, as businesses can invest in research and development.

The Adaptation Plan’s commitment to preparation and response, including community resilience, can help identify and protect assets at risk of extreme weather events, benefiting forestry businesses, land-based industries, and rural businesses and infrastructure exposed to wildfire risks. The increase in community engagement and education will help promote the risks of wildfires, in turn reducing the risk of economic losses and the potential loss of heritage assets.

Understanding climate scenarios in relation to UK and European building standards could reduce climate related risks and disruption to businesses situated in new buildings. Actions to support climate resilience in new and existing buildings will result in reductions in climate related risks and reduce disruption to businesses located in existing buildings. While resulting measures can result in increased costs for building developers, there are also anticipated benefits to achieving net zero emissions and providing jobs by incentivising the construction sector to increase demand for labour (Royal Institute for Chartered Surveyors, 2020). There are also anticipated social benefits such as health benefits to homeowners, through the reduced risk of overheating, and the associated lower or avoided treatment costs from overheating, affordability through the potential for lower heating bills, and a reduced risk of flooding in homes for homeowners (UKGBC, 2021).

The Adaptation Plan’s provision of more guidance, support and grant programmes will increase energy measures in buildings in Scotland, including historic buildings and heritage assets.

Additionally, lower climate risk in new and existing buildings ensures continued and affordable insurance for businesses in at risk buildings.

With regard to adaptation actions to make the historic environment more resilient, there is a potential for the provision of skills and training in relevant communities. There are also benefits for business located within historic buildings and businesses dependent on the wider historic environment such as tourism businesses, through a more sustainable cultural sector.

Outcome Three: Public Services

Developing guidance on climate change duties and continued support of public sector organisations will improve co-ordination and action for adaptation and resilience measures.

The enhancement of critical infrastructure and improving the resilience of essential services will have significant benefits for all sectors of the Scottish economy in the face of climate events.

Actions for a more resilient health and social care system will have benefits for Scotland’s economy through a healthy working population and benefits to businesses in the health and social care sectors.

Design advice for new schools will have medium-term benefits in maintaining an educated workforce.

An engagement with the UK Government on energy market arrangements has the potential to provide benefits for businesses in the energy sector and Scottish businesses by helping maintain secure and reliable energy supplies.

It is anticipated that the development of a Trunk Road Adaptation Plan and collaboration with Trunk Road companies to manage disruption risks, will have benefits for supply chains and businesses dependent on the movement of goods and the transport of people through improved adaption and resilience.

Ensuring Scotland’s railway network is up-to-date on adaptation and resilience alongside engagement to support future climate-related specification and development will benefit supply chain networks and businesses dependent on the transports of people and goods.

Increased promotion, information, guidance on resilience, interventions, and opportunities to Scotland’s maritime network and canals, will potentially result in increased climate change resilience resulting in benefits to dependent businesses and supply chains.

In relation to Scottish waters, securing future service resilience for customers will benefit communities and businesses dependent on water supplies.

A new National Flood Risk Assessment (NFRA) will help identify flood risk communities, businesses and infrastructure which will improve flood risk resilience and adaptation, and increased promotion and education on flooding will provide information and best practice guidance for at risk businesses and communities. Furthermore, collaboration with organisations will streamline flood risk management nationwide.

Outcome Four: Business and Industry

The Adaptation Plan objectives to increase the awareness of climate risks, as well as increasing support and advice for business preparedness and resilience, will prompt adaptation across businesses, leading to avoided cost (cost of inaction) associated with climate change and extreme weather events such as flooding, overheating, wildfire, water shortage. The Adaptation Plan aims to increase information dissemination regarding climate change adaptation with businesses. This can attract investment and further research can bridge information gaps regarding the impact of extreme weather events on the built environment, including flooding, extreme temperatures, high winds, and lightning strikes. It is stated in the CCRA3 that the cost of adaptation measures across rail and road networks is usually offset by improvements to repair costs and travel time delays.

The climate change risk assessment identifies flooding as the costliest climate-related risk to business in Scotland. As such, improved forecasting and flood resilience strategies will help to identify the businesses, communities and infrastructure at risk of flooding, and provide resilience strategies to inform adaptation methods. The adoption of sustainable strategies by local government can lead to beneficial changes to business models along with benefits to people from amenity and sustainable transport infrastructure. For example, climate resilient transport infrastructure will allow new developments to be connected to existing transport infrastructure, such as railways. Incorporating adaptation and resilience in policy and adaptation plans, as well as promoting awareness of interventions and opportunities, has the potential to further reduce risks and inform related businesses and sectors of available opportunities for adaptation.

Monitoring Scotland’s water resources will help provide practical advice to businesses on managing water scarcity, thereby raising awareness and reducing the risks associated with water shortage.

Actions to provide advice, skills and funding to support Scottish agriculture to take action on climate change adaptation, and research into Scottish crops and livestock will provide longer term benefits as agriculture becomes more resilient to climate change and more able to maintain production and profitability as the climate changes and severe weather events occur.

Funding research into the impact of climate change and extreme weather events (such as drought and waterlogging) on pests and pathogens of Scotland’s economically important crops, will deliver evidence-based strategies for crop protection, providing benefits to the agricultural sector as farmers are more able to avoid the climate-related impacts of pests and diseases. Research and development and better coordination between government and Scotland’s sectors could help to mitigate the risk to, and potentially enhance, productivity including integrated soil and water management, habitat restoration, and flood risk management, encouraging innovation and diversification. Investment into research can address productivity gaps and explore synergies that can be delivered through the improved use and management of land such as low carbon farming, improved nitrogen-use efficiency, and enhanced soil quality measures.

The delivery of the resilience action plan, more adaptation resources and support, and more investment in forest surveillance, has the potential to result in a more resilient forest sector, better able to maintain timber production and profitability as the climate changes and severe weather events occur. The Adaptation Plan will increase investment in nature based solutions for climate adaptation. This will have a positive impact on biodiversity and habitat restoration. This, in turn, will benefit the farming, fishing and forestry sector, food and drink industries, tourism, and businesses that rely on natural resources. Scottish Government social research shows that the public and private investment required to address the nature finance gap for Scotland of £12.5 billion would generate an estimated output effect of £17 billion into the Scottish economy. This means that every £1 invested would generate £1.35 for the economy. In terms of jobs, the same research finds that potential economic impact could be 146,020 direct and 197,380 direct and indirect jobs created or existing jobs sustained likely in industries such as silviculture, renting and leasing of agricultural machinery and equipment, and support services to forestry and hunting (SG, 2023). Additional further assessments will identify opportunities for changing forestry practice in relation to continuous cover, changing species, and INNS control.

Scotland’s freshwater habitats are vital for socio-economic development, food security, and biodiversity, with direct impacts to people and businesses, as research suggests that the overexploitation of ecosystems without regeneration has led to massive deterioration with consequences to human health, livelihoods, and biodiversity (Bogardi et. al., 2020). As such, research and policy development for best-practice science and management will have direct benefits, especially with regards to Scottish wild salmon and agriculture, through coordinated evidence-based scientific research and modelling to inform contemporary management. The development of Fisheries Management plans will help maintain sustainability of fish stocks and respond to changes in the status of stocks for fishing industries. More sustainable management measures will lead to a more resilient fishing and aquaculture sector, better able to maintain production and profitability with the changing climate.

Actions to increase research to identify the market demand and opportunities, supporting climate adaptation, will likely increase opportunities and support for the research and education sector, as well as downstream economic opportunities and benefits. Further research on the implications of projected climate changes within the context of potential changes in trade and other drivers will also help inform planning. There may also be benefits from more integrated cross-sector action across agriculture, forestry, natural environment, and human health to implement good practices and share tools and resources.

Actions to support regional development through enterprise agencies will deliver benefits for businesses in adapting. The development of an approach to regional just transition plans is likely to include a focus on businesses most likely to be affected by climate change and the transition to net zero.

Incorporating climate resilience specifically in supply chain risks will provide benefits to all businesses by helping ensure that supply chains are more resilient to climate change and climate events. Similarly, considerations for climate resilience and vulnerabilities in international supply chains will have similar benefits.

The Adaptation Plan objectives to improve Scotland’s domestic and international food security from climate-related shocks and the provision of funding to support the delivery of the strategy, with specific supply chain security considerations, will have benefits to food processing, wholesale, retail and catering/hospitality businesses.

Support from Transport Scotland to manage risks to business distribution networks from climate-related events will be beneficial to businesses dependent on the movement of goods and people because of greater resilience and adaptation to climate risks.

Actions to support greater resilience in public sector supply chains through the consideration of adaptation in supplier procurement contracts will encourage businesses supplying the public sector to adapt and become more resilient.

Outcome Five: International Action

The Adaptation Plan objectives to improve engagement and participation and the support for the development of the global evidence base on addressing non-economic and slow-onset loss and damage, will likely improve adaptation engagement and improve Scottish reputation globally with respect to climate related issues.

Business Consultation Responses

Benefits of adaptation

With regards to the benefits of increasing adaptation measures, respondents state that there will be specific opportunities for sectors like forestry, in relation to nature-based solutions, meeting retailer demands for accreditations and quality marks due to consumer demand, and increased resilience, and the related cost savings and reduced recovery time. Additionally, benefits will extend to communities through improved flood defences and marine management, as well as broader readiness for climate-related challenges. Overall, adaptation measures offer advantages in the short, medium, and long term, fostering business resilience against crises and unknown risks, including disease outbreaks and supply chain disruptions due to increased temperatures.

Opportunities of climate adaptation

It should be noted that respondents also highlighted potential opportunities as a result of increasing climate change adaptation including:

- innovation in areas such as building resilience, land use management, green-tech innovation in the financial services sector, growth in the renewable energy industry,

- the development and application of earth observation technologies, water purification technologies, agritech solutions for climate-resilient seeds/plants/trees, and opportunities for specialist consultancy and engineering services.

It is also anticipated that there will be collaboration across sectors to leverage opportunities for market development, increased productivity, lower carbon emissions, and landscape resilience. There are also anticipated opportunities arising as a result of climate change such as the potential increases in fish stocks like tuna, and the possibility of new shipping routes opening up through the Arctic, potentially shortening distances for trade.

Costs

This section sets out the costs of the Adaptation Plan. The assessment of the costs considers two options including a business-as-usual option where SCCAP2 is not updated, therefore, considering the cost of inaction, and the cost of adaptation where the SCCAP2 is updated to the Adaptation Plan following the European Environment Agency’s methodology for assessing the costs of climate change adaptation.

There are no aggregate estimates of the costs of adaptation for the UK, and thus no reliable estimates of adaptation finance needs. As such, the costs provided in this section are largely indicative.

Option 1 – Business as Usual (costs of inaction)

This option represents the cost of inaction where the current Scottish Climate Change Adaptation Plan is not updated.

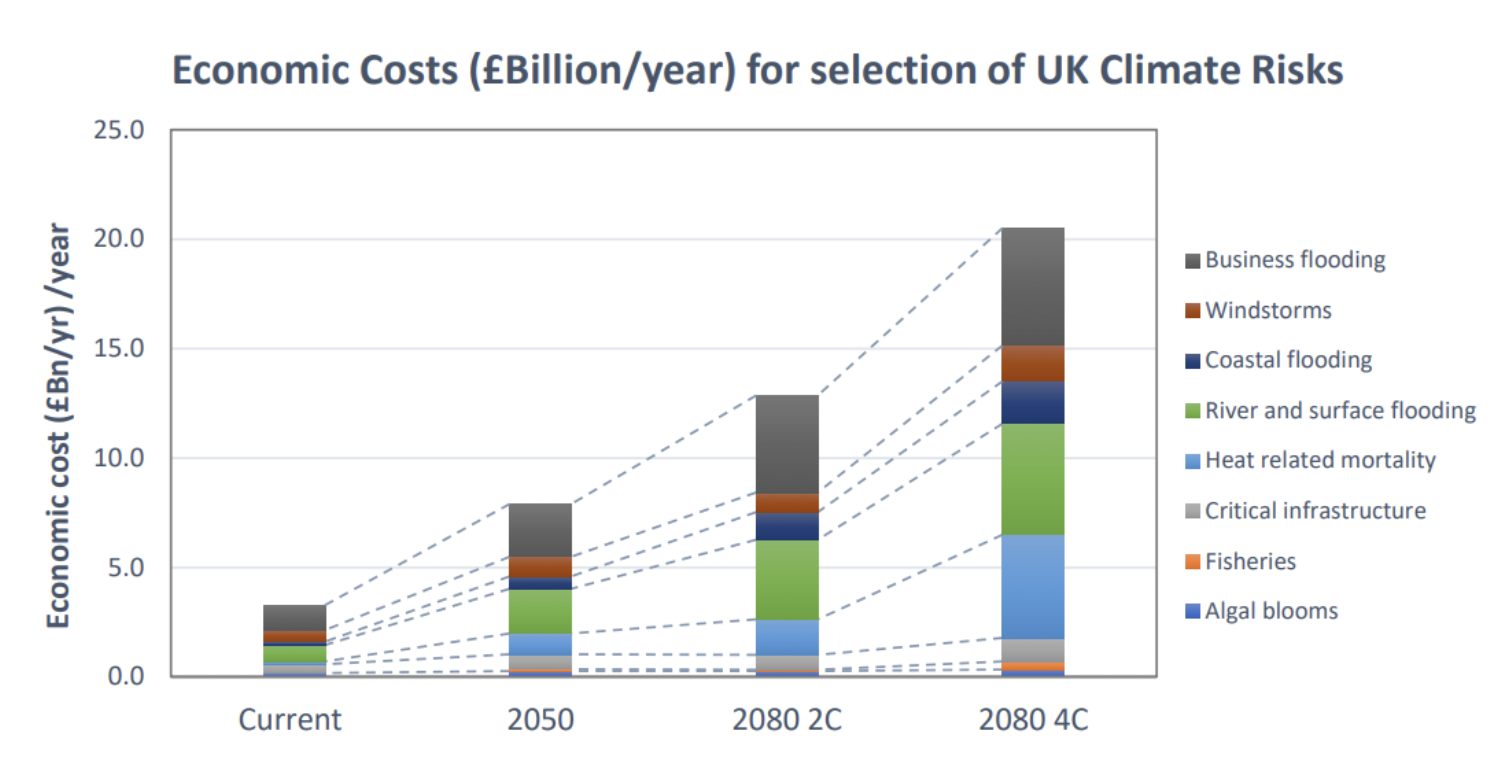

The impacts of climate change including extreme weather events and weather and climate variations is expected to increase as such under a ‘business as usual’ option. Evidence suggests that the potential for more extreme temperatures, weather and climate variations, and extreme weather events could exacerbate climate impacts to the Scottish public, economy and sectors. As such, it is estimated that the costs from climate change impacts in the UK are expected to increase under current climate projections with a variation in costs under a 2°C and 4°C scenarios (see Figure 3).

It is expected that estimated costs will vary with regards to Scotland. However, the outlined sections below present an indication of the costs to the Scottish public, businesses, economy and environment.

Cost of inaction to Scotland’s infrastructure and infrastructure services

Climate change impacts such as extreme temperatures, high winds and increased frequency of lightning strikes from more frequent storms impact many sectors of the Scottish economy and the Scottish public. This includes transportation and distribution networks where rail buckling, sagging overhead cables, signal failures, damage to equipment, thermal loading on bridges and pavements, loss of tree cover, transport disruptions, and delays in maintenance, have affected the sector (CCC, 2021). Between 2006 and 2016, UK-wide costs associated with these identified hazards amounted to over £20 million in compensation payments in relation to high temperatures, approximately £145 million in compensation payments for high winds related hazards, £40 million in compensation payments because of lightning strikes. Impacts to the built environment are of concern as the economic costs of indirect/cascading impacts have been estimated to be between 1.3 and 3 times the direct impacts of infrastructure failure and 5 to 6 times increase is estimated for a 2050 4°C scenario compared to the current baseline.(Watkiss, 2021).

Cost of inaction for flood risk

The risk of flooding to people, communities, businesses and the built environment is one of the most severe risks from climate hazards identified in CCRA3. The CCRA3 states that the economic impacts individually for residential properties from all sources of flooding in Scotland are estimated to be just over £68.5 million per year and the 2018 National Flood Risk Assessment for Scotland estimated that 284,000 properties are at risk of flooding. When including non-residential properties and indirect as well as direct damages, this estimate rises to £200 – 250 million per year. For instance, the storms of early 2016 were estimated to have cost the Scottish economy £700 million (CCC, 2021). However, the costs from flooding go past direct damages, to include consequential business disruptions, supply chain shocks, welfare effects such as health and wellbeing impacts, and the degradation of ecosystem services which can equal or exceed direct damages. The costs associated with flooding extend to other aspects of the built environment (O’Donnell et al., 2020). For example, it was reported that the Lancaster winter floods of 2015/16, had cascading impacts on communication services, transport and businesses, and the lightning strike-caused power outage in 2019 affected train operating companies, hospitals, water treatment plants and an airport. These impacts are also strongly linked to other sectors, interacting with other facets of the Scottish economy and people, including food, water, and health and community.

Cost of inaction to the rural economy

Climate-related impacts like damage and maintenance delays will increase threefold in Scotland. The potential for overheating in workers could increase eight-fold according to the CCRA3. It is also estimated that the annual cost of buckling and quadrupling of temporary speed restrictions, impacts to road services and network users from extreme temperatures, and clear-air turbulence during the cruise phase of flights is projected to increase because of climate change, increasing journey length and fuel consumption (CCC, 2021). The expected increase in risks under projected climate change may lead to reduced growth and reduced carbon sequestration, potentially affecting the competitiveness and profitability of food and other products for businesses and consumers. It may also increase capital costs, such as new machinery and technologies that reduce the environmental impact of farming/land management as sectors, households and businesses both at home and abroad may need specialised services and skilled trades to adapt to the changing climate.

The impact of extreme weather events like flooding has the potential to affect access to capital for businesses as the availability and affordability of insurance cover will be affected by rising risk levels. As such, credit may become more expensive for companies who are considered to be taking insufficient action to adapt to climate change or business at more risk to climate change impacts, such as business in high flood risk areas. A business’s ability to adapt may also be limited by the availability of affordable loans to finance adaptation measures.

The changing climate is also likely to have direct impacts on business and employee productivity, as well as the health and wellbeing of the Scottish people because of heat stress. Workers engaged in particular sectors or occupations, such as builders, farmers and factory workers, who are involved in manual labour, may be at the greatest risk of heat stress. Extreme weather can also impact productivity because of travel and supply chain disruptions, which could lead to increased costs and reduced reliability for consumers. There could also be increases in maintenance costs for wear and tear of vehicles from melting asphalt and cracking pavements, and fuel consumption because of air turbulence.

Additionally, analysis suggests that the avoided decrease in residual damage costs because of coastal adaptation is likely to be significant, resulting in additional avoided costs for business premises (CCC, 2021).

There is also evidence to suggest linkages between water resources and socio-economic development (Báldi A and Vári A, 2019).

Cost of inaction for invasive species

Pests and invasive species will have negative impacts on Scotland’s farming, fishing, and forestry sector and cascading effects for the food and drink industry and tourism industry. Affected species and habitats will involve native and non-native species respectively, and can lead to food shortages, can affect the affordability and the health and wellbeing of people living in Scotland. Indicative estimates of the economic damage from pests, invasive, and non-native species, suggests that this impact potentially costs £1.8 billion per year to the UK economy and £0.24 billion per year to the Scottish economy (CCC, 2021).

It should be noted that there could be potential benefits from new species populations because of invasive species which could reduce the cost to the Scottish economy and relevant sectors (CCC, 2021). This includes the rising populations of species and habitats that will thrive in rising temperatures the northward migration and expansion of species towards new areas. However, it is not yet possible to provide a valuation of this benefit. Other benefits that could offset some of the costs to the agricultural and forestry sectors arise from changing conditions that favour agricultural products such as improved suitability for wine growing and increases in tourism as other international regions are affected negatively from climate change (Watkiss, 2021).

Cost of inaction for the farming and fishing industry

The impact of flooding also extends to the agricultural sector where evidence shows that the area of best quality agricultural land at risk from fluvial flooding in Scotland is projected to increase by 26% by the 2050s and 31% by the 2080s under a +2°C at 2100 scenario (CCC, 2021).

Weather and climate variations also affect utilised land area, yields and productivity, and climate projections show that existing good quality land would become less suitable for arable uses because of drought risk and excess waterlogging which could be a greater current risk than water or heat stress for wheat yield in Scotland. Additionally, weather and climate variations, in combination with other factors, have negative impacts on soils. Future projections show that the risks to soil and Scottish agriculture and forestry businesses is likely to increase because of heavier rainfall events, resulting in erosion, compaction, and pollution, and increased soil moisture deficits in summer, leading to loss of soil biodiversity and organic matter. The estimated economic impact to Scotland, is estimated to range between £31m and 50m per year from soil erosion by water. This risk to Scotland’s farming industries could have potential international impacts such as risks to food availability and risks to the financial sector from price shocks, which could have very high economic costs (Watkiss, 2021).

Further impacts to both the natural and built environment in Scotland include reduced water availability and higher temperatures, which could affect freshwater habitats and Scotland’s buildings and business. For instance, salmon migration in rivers has been found to be correlated with freshwater temperatures, which is of national and international importance in Scotland, accounting for significant portions of UK and European salmon production (CCC, 2021).

Option 2 – Implement the draft SNAP (the cost of implementation)

Under this option, it is anticipated that there will be additional costs because of the implementation of the outcomes of the Adaptation Plan but also benefits resulting from climate impacts avoided and climate opportunities realised. The costs associated with this option have been collated from available evidence and analysis from various sources to provide high-level estimates of potential costs.

A recent report from Watkiss on the costs and benefits of climate change adaptation in the UK states that:

“Estimating the costs of adaptation at national and local level is extremely challenging.” (Watkiss, 2022)

In this assessment, we have attempted to give a perspective on the costs and benefits of the proposals included in the draft SNAP. To achieve this, we have relied on secondary sources, along with professional judgement, to provide quantification of costs and benefits where possible. It is also worth highlighting that adaptation is likely to include high operating expense costs (recurring, associated with ongoing operations, maintenance, etc.). It is important to note that the cost and benefits are not likely to fall evenly across the business sector. Costs may be front loaded and benefits are likely to accrue over time, particularly as climate change becomes even more pronounced. There are also likely to be disparities in the geography of costs and benefits, with some of the benefits difficult to predict given the spatial variation in severe weather events. Furthermore, some geographic areas are more likely to be affected by different types of climate risk.

Furthermore, a report from Watkiss states that:

“There will be costs associated with addressing climate risks with business supply/supply chains, but these are not well characterised. There are some case studies on the costs of adaptation for addressing labour productivity impacts.” (Watkiss, 2021)

Therefore, the costs of climate adaptation on businesses is a relatively unexplored topic.

There is limited evidence to undertake a valuation of the Adaptation Plan against SCCAP2 and uncertainty surrounding the economic impact of previous adaptation plans as such the costs of adaption presented are largely indicative and qualitative in nature, informed by available literature.

The future actions of the Adaptation Plan are wide reaching, and there is a strong economic case for greater Scottish Government intervention in research, policy development, monitoring, awareness, and coordination of reactive responses. While the costs of adaptation may largely be absorbed by land owners, consumers, and relevant sectors, it is anticipated that the economic benefits of adaptation are high compared to the costs (Watkiss, 2021). It is important to note that the implementation of funding and grants will help reduce the impact of costs while the provision of research and strategies will streamline information and management practices needed for climate change adaptation across sectors.

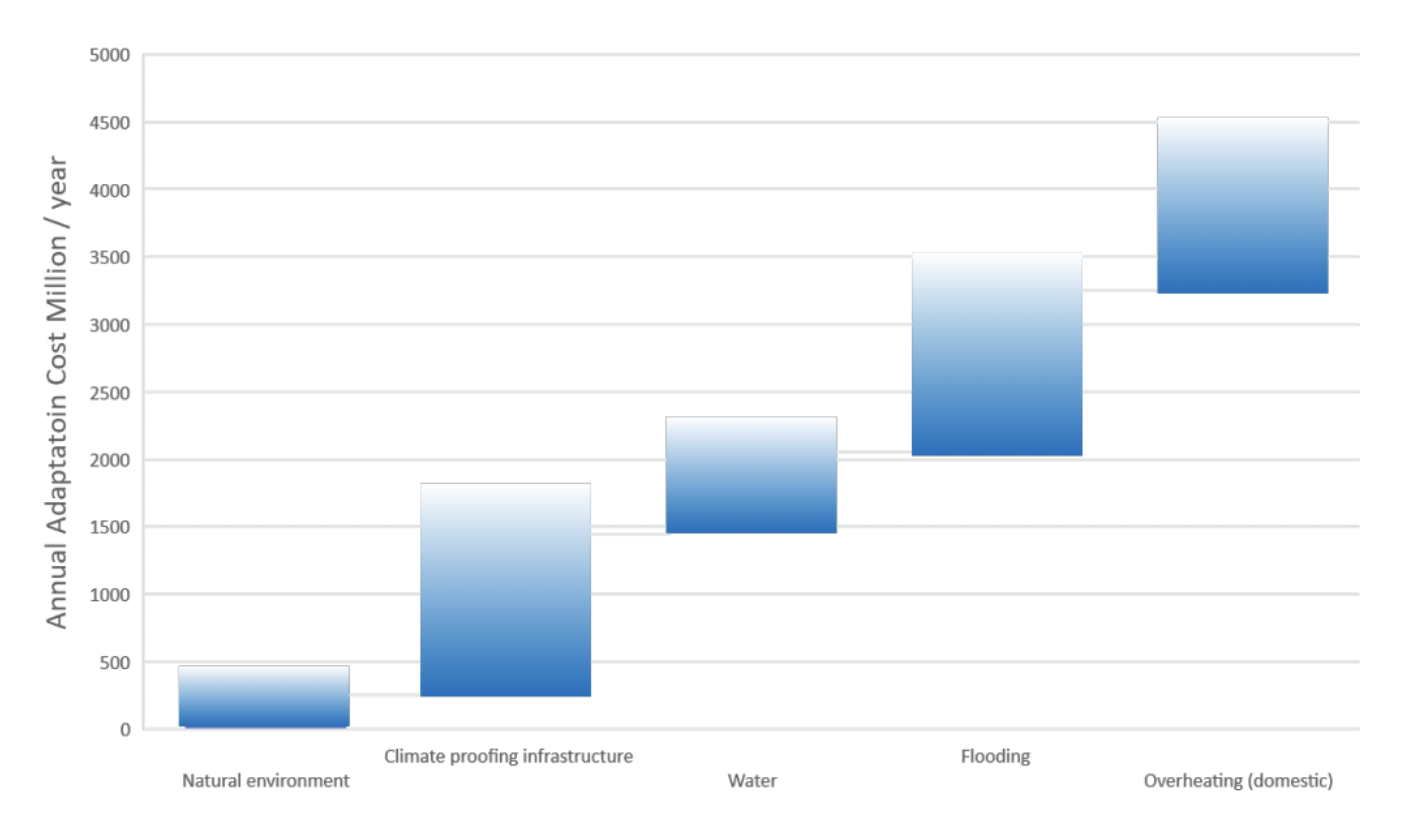

While it is difficult to anticipate the economic cost of the Adaptation Plan for the Scottish public, businesses and third party sectors, exact costs will depend on a variety of factors, including the specific measures. However, an initial review of the costs of adaptation for the UK indicates adaptation costs / investment needs for nine important CCRA3 risks might be around £5 billion to £10 billion a year for this decade (Watkiss, 2022). It is expected that these estimates are likely to increase as the severity of climate change impacts increase. Figure 4 presents the indicative costs of UK adaptation for the major risks in the CCRA3 UK from this review.

It is also important to note that these costs can be offset by the benefits of adaptation, including actions implemented by the previous Adaptation Plan (SCCAP2) which have long-term effects such as reduced damage from climate events, improved health because of cleaner air, and economic stimulation through current and future investments.

Outcome One: Nature Connects

With regards to nature-based solutions, potential changes and restrictions on land use and land management practices could affect some businesses and potential restrictions on water abstractions and discharges could have a similar effect.

The CCRA3 Cost of Adaptation and Economic Costs and Benefits of Adaptation in the UK report estimates that the finance gap for UK nature to deliver nature-based outcomes and targets could be £44 billion and £97 billion over the next 10 years. The same report suggests that considering further impacts of delivering UK climate change targets could add to the risks assessed in the CCRA3, these costs could increase by 20% (Watkiss, 2022). These costs will be potentially high for the farming, agriculture and forestry sector and the Climate Change Committee states that Scotland’s agricultural sector is particularly vulnerable to the impacts of climate change (CCC, 2023). However, these costs have been described as low regret options, especially for dependent industries like the food and drink industry.

Actions to provide mapping support could potentially create restrictions on land use from new information which could impact related businesses.

It is anticipated that the resulting projects from increased investment into BGI and marine restoration and enhancement could potentially result in short-term restrictions on fisheries as well as restrictions on future marine energy development.

The Peatland Action Plan and the review of UK Forestry Standard has the potential to result in changes in land use, allowing peatland restoration and woodland creation and expansion.

Outcome Two: Communities

It is anticipated that increased and improved coordination between public, private, and third sector to support adaptation and resilience will require increased time inputs and costs.

The Adaptation Plan’s resilience objectives could result in restrictions on land and/or land use.

There could be potential increases in design and construction costs for new buildings as a result of updates to building standards from understanding climate scenarios in current British and European standards, and there are costs of retrofitting adaptation measures to existing business premises. Retrofitting is a crucial step towards achieving Scotland’s net-zero carbon goals, however, expert insight suggests that retrofitting Scottish buildings is a long-term project, is time and resource intensive, and will result in pressures on human resource capacity and budgets for repair and renovation (Scottish Parliament, 2021).

As part of CCRA3 evidence conducted by Paul Watkiss Associates, an analysis on typical uplifts associated with climate proofing showed that the annual adaptation cost of building climate resilience in the UK’s National Infrastructure Delivery Plan (NIDP) economic project pipeline could be £0.2 billion to £4.8 billion/year, with a central estimate of around £1 billion/year (Watkiss, 2022).

It is anticipated that there will be added considerations for the development of new buildings and infrastructure in Scotland because of policy changes and as more sustainable strategies are developed which could result in initial cost loading. However, a significant portion of these costs will be offset by avoided cost from more climate resilient infrastructure and buildings.

As the climate changes, individuals, households, and businesses will need access to new products to help them adapt to the changing climate. This will include emerging markets for new products and services such as those required in construction for more resilient buildings, from potential new building standards from understanding climate scenarios in current British and European standards, and skilled workers required. Emerging markets for new products will develop from changing consumer demand for existing products in response to climate change (Tao, 2022).

The CCC’s Costs of Adaptation and the Economic Costs and Benefits of Adaptation in the UK report sets out some of the housing-related costs of adaptation. It is anticipated that there will be additional adaptation costs at the UK level because of the scale up needed to address the risk of overheating. These costs will extend to both residential and non-residential buildings, and are likely to be high. For example, the indicative costs for mechanical cooling systems in new buildings are between £1000 - £3,000 per house, or £0.2 – £0.9 billion/year for 200,000 to 300,00 new homes a year. While retrofit costs are anticipated to be much higher. The CCC provides an indicative estimate for climate proofing building stock in the UK at £4-5 billion overall by 2050 (Watkiss, 2022).

The adaptation actions to make the historic environment more resilient will lead to economic costs of retrofitting adaptation measures to existing business premises and there is the potential for the costs of adaptation to impact some cultural sector businesses.

Outcome Three: Public Services

Improved identification of flood risk communities and areas could lead to future restrictions on locations where development will be permitted and guidance and information on flood risk will lead to additional considerations and retrofitting costs for at risk business properties and communities.

Outcome Four: Business and Industry

It is not clear what the direct economic costs of adaptation will be for related Scottish businesses. However, it is anticipated that research and policy development into the various actions of the Adaptation Plan regarding the natural environment will lead to significant changes in operational and management practices and the promotion of information and adaptive measures will likely lead to behavioural changes in the Scottish consumers.

It is anticipated that adaptation, and the associated costs of adaptation, prompted by increasing awareness, will most likely be focused at risk areas like coastal regions and small businesses in Scotland. This is also applicable to areas of water stress regarding the risk of water shortages.

Additional advice, skills and funding, as well as new research for the farming and wider agricultural sector will potentially result in changes in the pattern of land management to anticipate climate change and avoid impacts.

Actions to improve the resilience of the forestry sector will result in additional spatially specific adaptation considerations and potentially result in changes in forestry practice and changing costs of management needed to respond to climate change.

Incorporating climate resilience specifically in national and international supply chain risks could lead to higher costs for businesses and consumers, however, it is anticipated that these costs will be outweighed by reduced risks to infrastructure and supply chain disruptions.

Funding and improved domestic and international food security from climate-related shocks could also introduce higher costs for businesses and consumers, though outweighed by reduced disruptions.

Actions to support greater resilience in public sector supply chains through the consideration of adaptation in supplier procurement contracts has the potential to lead to additional costs and considerations for tendering for public sector business.

Outcome Five: International Action

It is not anticipated that the Adaptation Plan objectives will lead to significant costs to Scottish people, businesses, and third party sectors.

Business Consultation Responses

Costs of adaptation

Respondents identified several key costs to businesses and industries in increasing Scotland’s climate change adaptation measures. These include direct capital-intensive costs, such as the expenses associated with implementing flood defences and other infrastructure, early adoption costs, such as trainings, until economies of scale are achieved, which could be particularly challenging for small and medium-sized enterprises (SMEs) facing capital expenditure considerations. Additionally, short-term disruptions to business continuity and limited capacity for smaller businesses to undertake climate adaptation actions were noted, along with the need for access to data and decision-grade data to understand climate-related impacts and risks.

Challenges of adaptation

Consultation respondents also raised concerns about costs and the potential for conflicting interests. They emphasized the importance of understanding climate-related risks at a regional level and the need for clearer information on adaptation funding and distribution. There was a call for more accessible data explaining climate risk to the public and improved modelling to assess the regional impacts of climate change within Scotland. Overall, there is a recognition of the complexity and interconnectedness of adaptation efforts and a need for better understanding, clarity, and action at various levels.

Distribution of costs and benefits

It was determined that the costs and benefits of adaptation will not be distributed evenly across Scotland. It was stated that geographically, areas facing the greatest risks, such as coastal communities and remote regions like Shetland, are expected to experience both significant costs and benefits, particularly in the fishing industry. Smaller businesses, with limited resources, are deemed less resilient and more vulnerable to the financial burdens of adaptation measures. Furthermore, forecast scenarios suggest uneven distribution of sea level changes and extreme weather events, leading to disparities in impacts across different regions and businesses. While there will be disparities in both costs and benefits, the impacts are expected to be more closely tied to markets rather than specific industries. Overall, SMEs and micro businesses are anticipated to face the greatest challenges in implementing adaptation measures, particularly in areas prone to climate-related crises like droughts and flooding.

Contact

There is a problem

Thanks for your feedback